Social Security at 89: Time to Retire the Old Benefit Formula

We should take a more holistic approach to reform

Today marks the 89th anniversary of Social Security. Like a stubborn senior, this program has been set in its ways for so long, you could be excused for thinking the Social Security Administration is still using rotary phones. Just as those phones have become relics of the past, it’s clear that Social Security needs a modern upgrade to reflect new demographic and economic realities.

Later today I will have the opportunity to address about 200 AARP members at the Ohio Social Security birthday bash, held at the Ohio Stadium in Columbus, with yet more members joining us for watch parties in other cities. The event has been sold out for days. You can register for the Facebook livestream if you’re eager to watch me spar with Max Richtman of the National Committee to Preserve Social Security and Medicare (NCPSSM).

During my remarks, I will emphasize that we need to take a more holistic look at Social Security and ask ourselves: what should be the goals of this ‘social insurance’ program? And then, how do we best accomplish those goals?

The Current Benefit Formula is Flawed

Opponents of benefit changes operate under the implicit assumption that current program design cannot be improved upon. But we have ample evidence that it’s time to retire the old benefit formula and replace it with one that more appropriately addresses the realities of 2024 rather than those that existed in 1935 when Social Security was introduced.

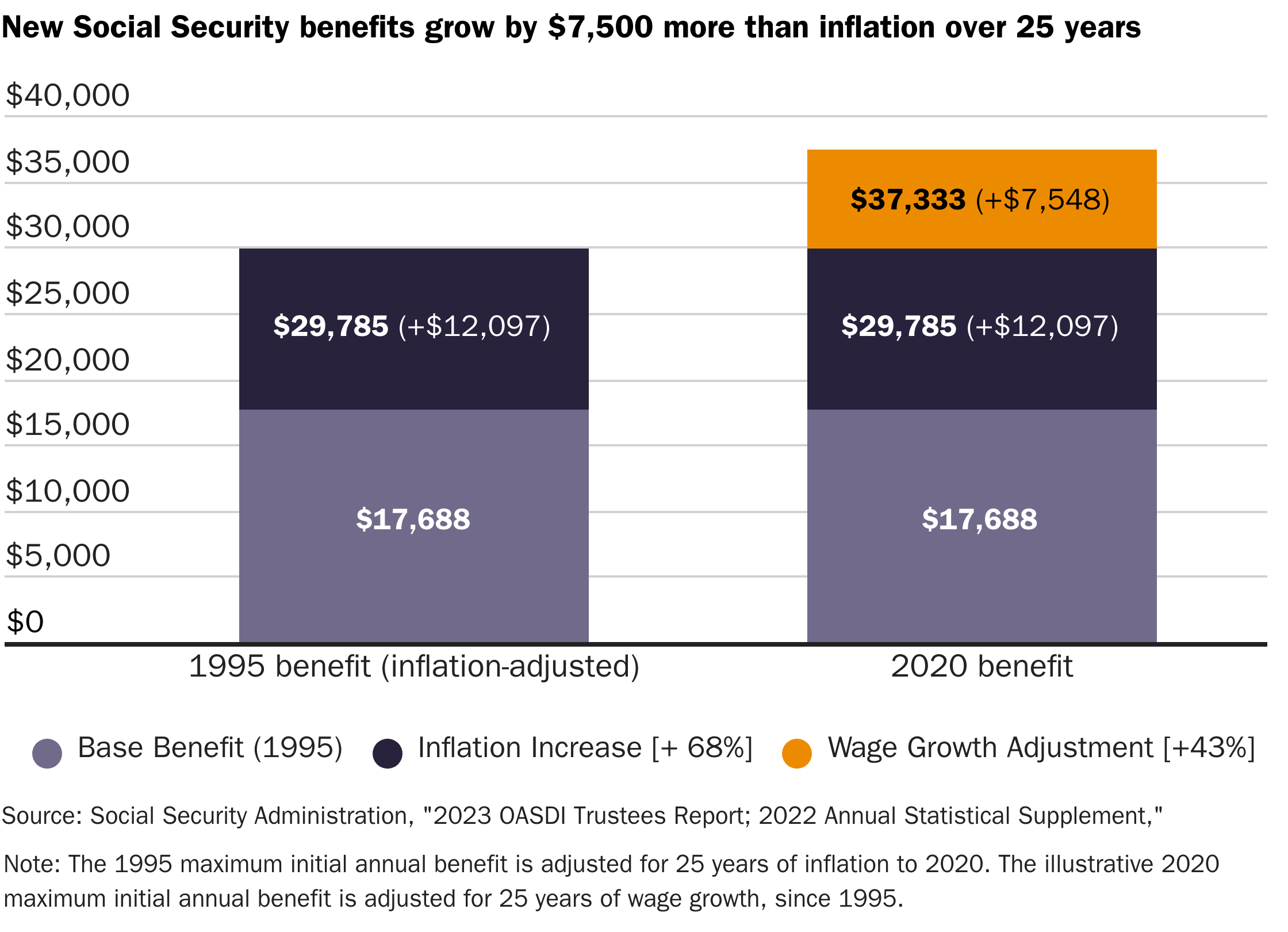

Current benefit design leads to many undesirable outcomes. For example, higher income earners receive excessively high benefits, with the highest-earning dual-income households able to collect in excess of $100,000 annually from a program that is funded by workers who tend to have lower incomes and net worth, on average. That’s redistribution in reverse, like Robin Hood stealing from the poor to give to the rich.

And because of how initial benefits get calculated when someone first applies for Social Security, two workers with identical earnings histories can collect vastly different benefits depending on the years in which they applied. That’s because benefits are only loosely tied to actual working histories and tax contributions. Initial benefits get a boost from economy-wide wage gains, such that someone applying in 2020 will collect $37,333 in Social Security, $7,548 more than someone with the same earnings and tax history who applied in 1995 (receiving $29,785 in 2020 instead). We can afford to protect current benefits from inflation (an increase in the general price level raising the cost of living) but we can’t afford ever-increasing benefits.

Noble Intentions, Flawed Execution

Social Security was established with noble intentions—to ensure that older Americans, those with disabilities, and survivors of deceased workers are not suffering in poverty. However, despite its success at reducing the overall poverty rate among seniors, the program’s financial structure is fundamentally flawed. Current workers pay for the benefits that retirees receive, and yet the benefit formula comes from an era when the number of workers paying in was far greater than it is today. America is undergoing a big demographic shift with older Americans living longer and collecting more Social Security over their lifetimes, as the number of working-age Americans funding their benefits is declining because people have fewer children than they did in the past. It’s because of this imbalance that Social Security has been running deficits since 2010 and is expected to add more than $4 trillion to the debt over the next nine years before the program’s borrowing authority runs out in 2033.

If Congress fails to act, the law dictates that benefits will be cut by 21 cents on the dollar for all recipients starting in 2033. If we make benefit changes now, we can avoid those automatic benefit cuts, without adding more debt or raising taxes. If we wait until closer to 2033, Congress will be forced to raise taxes on the workers paying Social Security’s bill. The alternative will be for Congress to pay the benefits with more debt, which in addition to burdening younger generations with higher interest payments could trigger higher inflation, which acts as a tax on everyone by raising the cost of living.

Effective Solutions Will Align Benefits to Better Match Revenues

In terms of effective policy solutions, eliminating the cap on payroll taxes sounds appealing but would hike higher earners’ tax rates to economically harmful levels that will take a toll on all workers by reducing their job opportunities and hampering the creation of new life-improving goods and services. Moreover, this approach only provides about five years of surplus revenues before returning Social Security to deficits, making it ineffective and unsustainable as a long-term fix. Raising the payroll tax for all workers is also untenable because it would raise the payroll tax burden of median wage earners, who make about $60,000, to $10,000 a year—an increase of $3,000 which many workers won’t be able to afford.

Instead, we should consider 1) reducing benefits for higher-income retirees, 2) adjusting the benefit formula to protect against inflation instead of growing benefits with wages, 3) modernizing cost-of-living adjustments so they are more accurate, and 4) gradually increasing the retirement age to reflect longer life expectancies. These changes would align benefits better with current demographic realities and encourage longer workforce participation, benefiting workers with a stronger economy and improving Social Security’s finances.

The real danger lies in Congress avoiding tough decisions and opting to borrow more to avoid scheduled Social Security benefit cuts in 2033. Such an abdication of fiscal responsibility would exacerbate the national debt and burden future generations with higher taxes and inflation. It could also send a dangerous signal to those buying America’s debt that we’ve become less credit-worthy, which would drive up interest rates and could trigger a fiscal crisis. It shouldn’t take a fiscal crisis to adjust Social Security benefits to better match the times.

As we reflect on 89 years of Social Security, it’s clear that the status quo is no longer sustainable. Reforming Social Security isn’t just about balancing the books—it’s about realigning the program to focus the government on what the government does best while otherwise leaving people free to work, save, and invest as they deem best.

I also understand that looking under the hood and feeling duped makes people angry. So I am not surprised about your reaction. It’s still important that we face the facts even if this makes us feel bad initially. We can’t afford to keep pretending Soc Sec is something that it is not.

It is not a savings program. It is not an investment. It is a government redistribution program and the only thing distinguishing it from all other welfare is that it has a dedicated funding source on paper that limits its borrowing authority in statute and applies limited meanstesting.

Government can keep seniors out of poverty as FDR promised but should otherwise leave Americans free to save and invest for their own retirement (which is something most rational people can plan for). A true social insurance program would insure against an unexpected event…like the disability program does. Getting old isn’t something that we can’t foresee although we may not know exactly for how long we can work as old age increases the incidence of disability.

Perhaps it would help to emphasize that Social Security has _always_ been a transfer from current workers to retirees. That’s not how it was sold. It was fine when the ratio of workers to recipients was 30 to 1. Last time I checked it was 3 to 1, and headed south.

The social security surplus was never invested. Congress wrote IOUs to itself and spent the money. The special T-bills in the filing cabinet in Virginia are worthless. President Bush was excoriated for pointing that out.

It’s as if you’re saving up for a new car. Every payday you write yourself an IOU, and spend the money you planned to save. When it comes time to buy the car all you have is a stack of worthless paper.