Welfare Digest | Fraud Risks in New York's Home Health Care Program

Links & Benefits Breakdowns

Here are this week’s links and benefits breakdowns:

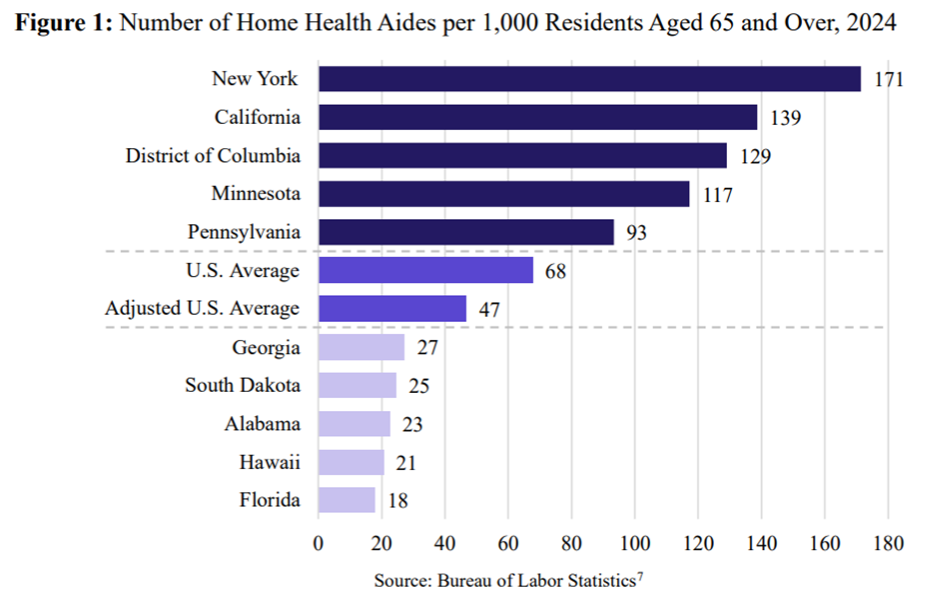

JEC Flags Fraud Risk in New York’s Exploding Home Health Care Program. A recent issue brief from the Joint Economic Committee (JEC) highlights that New York has 171 home health aides per 1,000 residents aged 65 and older, almost triple the national average. One reason for this is a lack of guardrails against waste, fraud, and abuse in the state’s Medicaid-funded home health care services, namely the Consumer Directed Personal Assistance Program (CDPAP) — which fell victim to a $68 million fraud scheme, as previously highlighted by the Debt Dispatch. As the JEC explains, CDPAP allows Medicaid-eligible individuals to choose friends or family members, even those with “little to no healthcare experience,” as caregivers. “Both limited standards to meet for an individual to be eligible for services and little to no training required for caregivers” have led to CDPAP spending expanding “well beyond what would be expected” given the state’s senior population. The program’s spending ballooned from $2.5 billion in 2019 to an estimated $12 billion in 2025, with the federal government bearing 57 percent of the cost. CDPAP’s rapid spending growth has persisted “despite attempts by the governor to reform what she has called ‘one of the most abused programs in the history of New York.’”

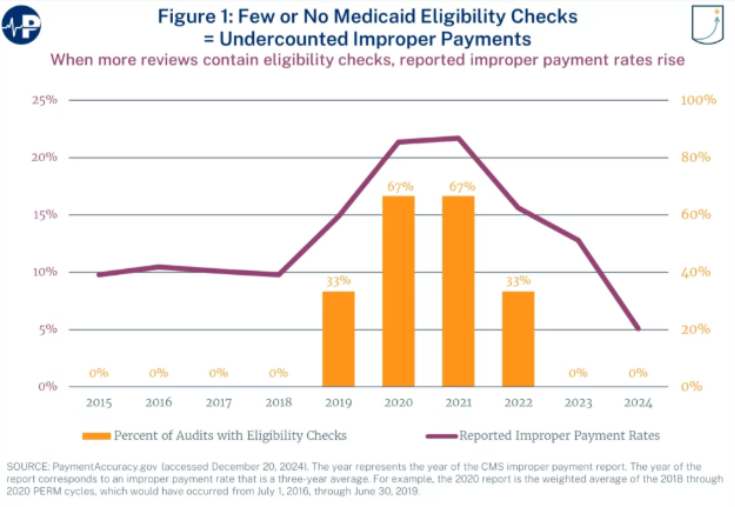

Medicaid's Real Error Rate Is Likely Far Higher Than CMS Reports. The Centers for Medicare & Medicaid Services (CMS) estimated that Medicaid's improper payment rate was 6.12 percent in fiscal year 2025. However, Paragon Health Institute scholars Chris Medrano and Brian Blase argue that the methodology behind this estimate is “crude and does not measure the amount of waste, fraud, and abuse in Medicaid.” As they point out, the Payment Error Rate Measurement (PERM) doesn’t fully account for eligibility errors, which “explode” the improper payment rate when measured properly. In 2020 and 2021, when CMS conducted eligibility reviews in two-thirds of states, the national improper payment rate exceeded 20 percent. PERM also does not examine managed care claims at the provider level, even though more than two-thirds of Medicaid enrollees are in managed care plans. This managed care gap “means that the program misses multiple errors,” such as payments going to ineligible providers and duplicative or undelivered services. “Given these limitations, PERM is not a good proxy for Medicaid misspending. It is a narrow, lagged audit of a subset of administrative errors.”

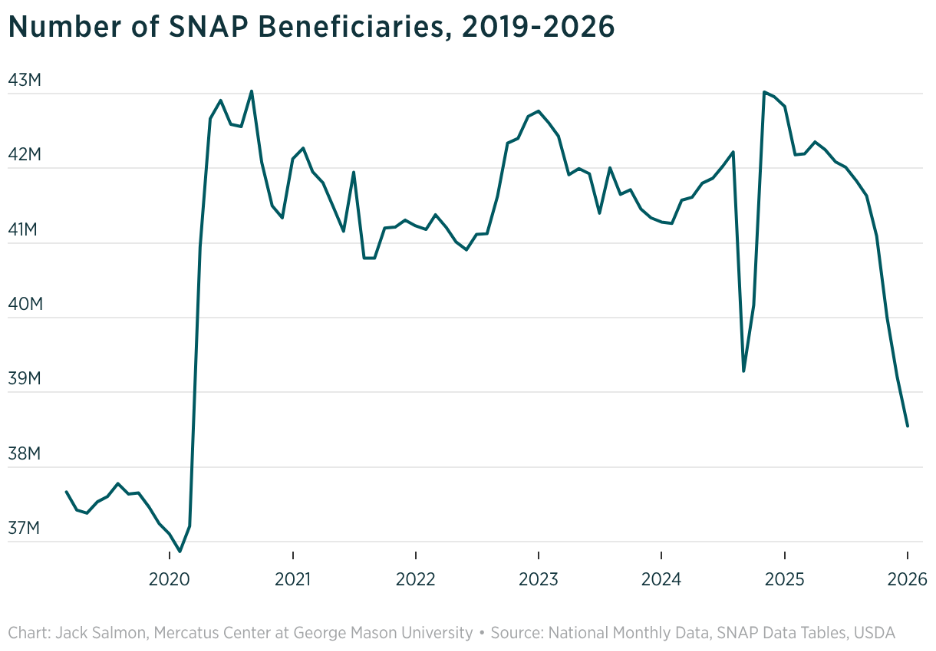

SNAP Enrollment Is Falling but Remains Well Above Pre-Pandemic Levels. For the first time since before the pandemic, the Supplemental Nutrition Assistance Program (SNAP) is “beginning to shrink back toward normalcy,” writes Mercatus scholar Jack Salmon. SNAP enrollment declined by nearly 4.3 million from January 2025 to January 2026, with roughly 3.5 million occurring after the One Big Beautiful Bill Act (OBBBA). Although enrollment had also been artificially elevated by COVID-era policies that suspended work requirements and weakened eligibility enforcement, OBBBA’s work requirement provisions were another “important explanation for the recent decline.” However, even after the bill’s reforms, “the program still remains substantially larger and more expensive than before the pandemic,” with enrollment still 1.7 million above pre-COVID levels. Although SNAP is beginning to “reverse” after years of welfare expansions, further reforms are needed to improve the “[program’s] integrity and long-term stability” and restore it to its intended role as “temporary nutritional assistance for vulnerable households.”

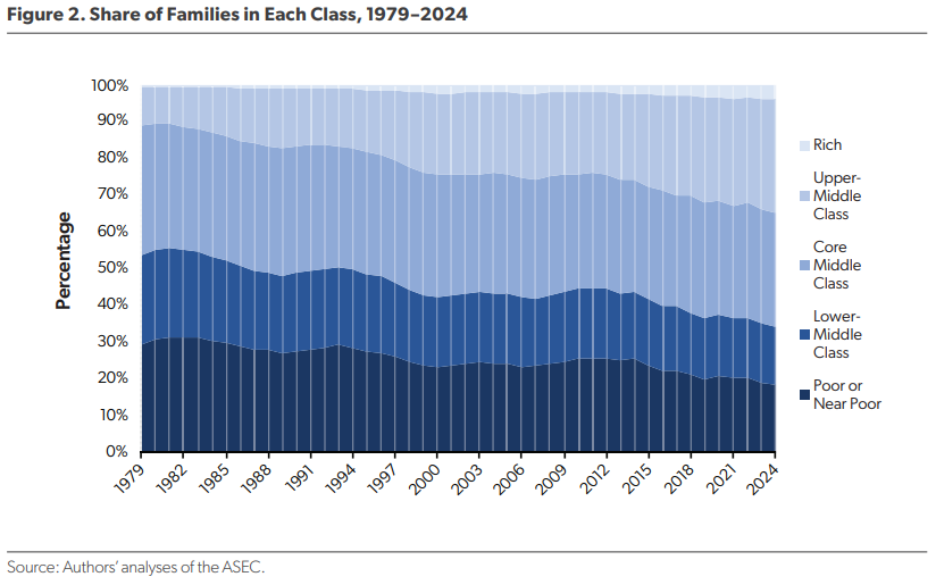

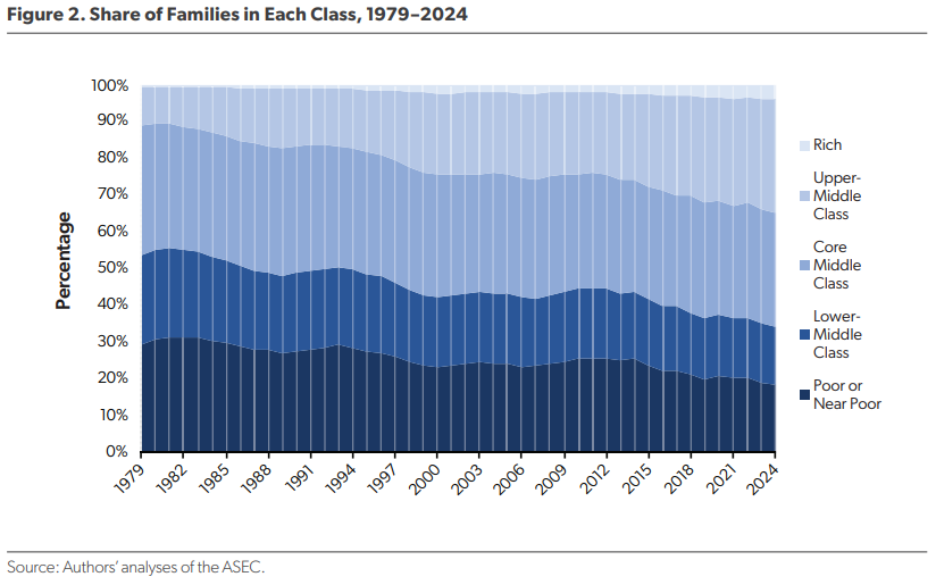

The Middle Class Is Shrinking Because of a Booming Upper-Middle Class. A new AEI report by Scott Winship and Stephen Rose finds that the American middle class has been shrinking not because families are falling behind, but because more are moving up. After grouping families into five income classes using absolute income thresholds adjusted for inflation and family size, Winship and Rose found that median family income rose 39 percent from 1979 to 2024 — 52 percent after adjusting for the decline in family size over the period. Although the core middle class shrank from 36 percent of total families in 1979 to 31 percent in 2024, this was entirely due to the middle class moving up the income ladder, with the proportion of families in the upper-middle class tripling from 10 percent in 1979 to 31 percent in 2024. “For the first time in American history, more families in 2024 were above the core middle class threshold (35 percent) than below it (34 percent).” As Winship and Rose put it: “What we see, then, is not a hollowing out of the middle class but a booming upper-middle class.”

Minimum Wage Hikes May Push Vulnerable Workers into Homelessness. In addition to reducing employment among low-skilled minorities, as the Debt Dispatch has previously covered, minimum wage laws may also exacerbate homelessness, according to a paper by political scientist Seth Hill. Matching average state and local minimum wage laws to homelessness estimates from the Department of Housing and Urban Development, Hill estimated that “a 10% real increase in the minimum wage leads to a two or 3% increase in the homeless population.” Although minimum wages might raise incomes for some, “they also trigger employment disruptions and negative income shocks,” which fall hardest on “the least competitive employees such as those struggling with mental illness, substance abuse, or unstable family support networks.” As Hill says, this means that the “negative consequences of minimum wages would fall disproportionately on those who already face a higher risk of homelessness.”