Debt Digest | Spooky Edition

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts.

Bond market’s ominous warning. Duke Professor Campbell Harvey explains, “[O]ver the past eight recessions, from the late 1960s to today, every time we got that upending of the bond market, where the long-term rate was lower than a short-term rate, a recession followed without any false signals — so eight out of eight. And so this is perhaps the most reliable indicator of what will happen in the economy…the yield curve inverted in November 2022…I wrote a LinkedIn post saying that this could be a false signal…But there was a very important caveat. I said, Yeah, I think we can dodge a recession, but it’s conditional on the Fed stopping their rate hikes. And that’s not what happened…the consumer is not going to be able to bail out the economy in 2024.

The interest cost monster. Lyn Alden writes, “The United States now pays more money on its interest expense than it does on its entire military. The mid 1990s to the early 2020s saw a great moderation in interest expenses, and this coincided with the opening of the Soviet Union and China and consequently a large period of disinflationary globalization. That period is over now...I view [the U.S. raising taxes or cutting spending] as being very unlikely to happen in today’s polarized political environment…So, in the long run I expect this to lead to persistent above-target inflation, or waves of inflation punctuated by temporary disinflationary slowdowns, driven by large monetized fiscal deficits.” Boccia explains the danger of using quantitative easing as a tool for financing government spending here.

Debt crisis surprise! Arnold Kling writes, “[A] debt crisis always comes as a surprise, and once it comes there is no easy way out.” “Just as a bank must make a guess about a credit card borrower’s willingness to repay under financial distress, investors in sovereign debt must make a guess about a government’s willingness to repay under financial distress. This in turn requires judgments about political incentives…The assumption that the United States will have the political will to stabilize its fiscal position is based more on hope than on recent experience. If the political process continues to enlarge the government’s commitments to spend in the future, investor expectations will change at some point. That change in market perception is likely to be swift and severe,” he explains.

Vampiric tax hikes. The Tax Foundation’s Erica York writes, “Tax-based deficit reductions tend to have a more negative impact on the economy and less successful track record than spending-based ones. The difference is primarily due to the response of private investment, as business confidence falls to a greater degree and for a much longer duration after tax-based plans.” “If large tax increases are self-defeating, it leaves spending cuts as the most effective way for Congress to address the budget crisis. Spending cuts are less likely to prolong recessions and can address the root cause of long-term deficits, uncontrolled spending growth,” explains Cato’s Adam Michel.

Light at the end of the tunnel. The Committee for a Responsible Federal Budget highlights a litany of budget process reforms. One promising option: “Fiscal targets as part of the budget process. Congress should adopt multi-year debt-to-GDP targets designed to gradually reduce debt as a share of GDP and keep it below 100% of GDP. Policymakers could further establish expedited procedures to help meet the targets along with budgetary triggers for enforcement.”

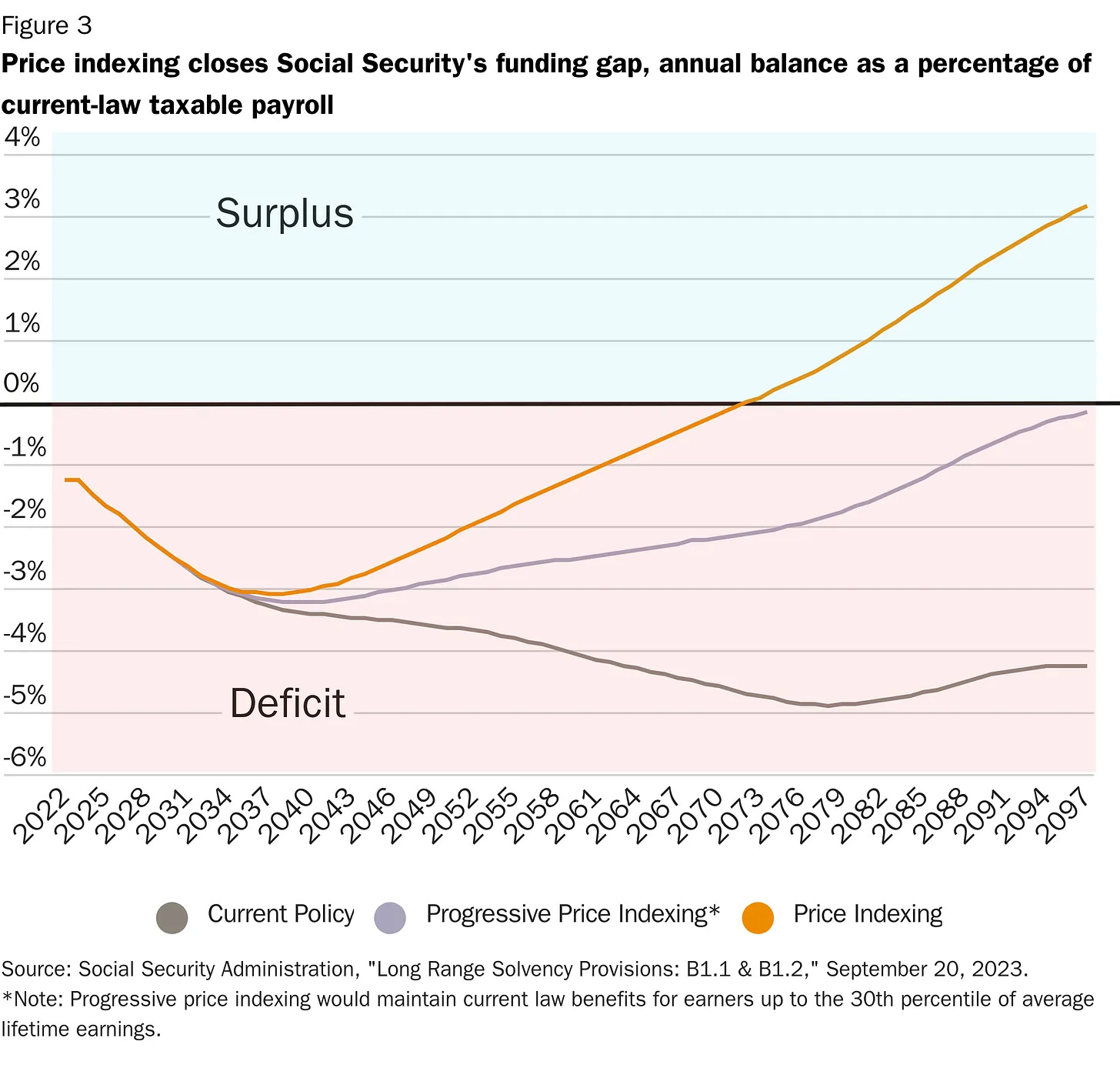

You can’t outrun the Social Security funding crisis. Andrew Biggs, John Cogan, and Daniel Heil write, “December 20, 1977…Had Congress acted differently on that day, by adopting the unanimous recommendations of a congressionally appointed expert panel, Social Security’s $22 trillion funding shortfall would not exist, and retirees would not face a 20 percent benefit cut when Social Security’s trust fund runs dry in 2034.” “It is not only possible to preserve Social Security benefit adequacy while slowing benefit growth, it is actually necessary if policy makers wish to avoid forcing participants into sub-optimal outcomes,” explains Mercatus Center’s Charles Blahous. Adopting price indexing—changing the initial benefit formula to account for inflation instead of wage gains—would protect beneficiaries from inflation and achieve trust fund solvency argues Boccia. The chart below compares Social Security’s projected funding gap under several benefit indexing options.