Debt Digest | Rising Debt Stifles Income Growth

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

Expanding HSAs could reduce healthcare costs. Rep. Chip Roy’s (R-TX) “Healthcare Freedom Act of 2023” would expand eligibility for health savings accounts (HSAs) to all individuals regardless of their health plan. The bill would exclude employer contributions to such accounts from gross income taxation and phase out the tax exclusion for employer-sponsored insurance (ESI). According to Paragon Health Institute, “HSAs are associated with lower health care spending,” with “One study [finding] that the introduction of HSA-qualified plans and HSAs was associated with a 15 percent reduction in total health care spending.” Furthermore, Cato’s Michael Cannon explained in an email exchange: “The American Academy of Actuaries estimate that ‘reference pricing,’ which is one tool for making consumers more price-sensitive, could trigger price competition that reduces prices ‘for shoppable services by 0 to 28 percent,’ which would amount to ‘0 to 12 percent of the spending for all services.’ If Rep. Roy’s bill would result in workers taking control of the $1 trillion of their earnings that employers now spend on ESI, that would make health care consumers dramatically more price-sensitive than reference pricing would. Therefore, those AAA ranges are a reasonable baseline for how much prices could fall if workers gained control over that $1 trillion.”

Why do governments resort to money printing? Thomas Savidge, a Research Fellow at the American Institute for Economic Research (AIER), explains why governments turn to “money printing” and borrowing to finance spending: “Policymakers have an incentive to finance spending with money printing and debt to hide the cost of spending from taxpayers. These costs cannot be hidden forever, though, as inflation and tax increases to pay for yesterday’s unproductive spending will eventually follow.” The latest episode when monetary policy served fiscal needs occurred during the COVID-19 pandemic, leading to rampant inflation and record-high deficits. As Dominik Lett and I have written: “If Congress leaves spending corrections to the last minute, legislators may perceive the draconian fiscal consolidation necessary to bring debt under control as less desirable than monetizing the debt. In such a scenario, printing more money might become the easiest or only politically feasible way out.”

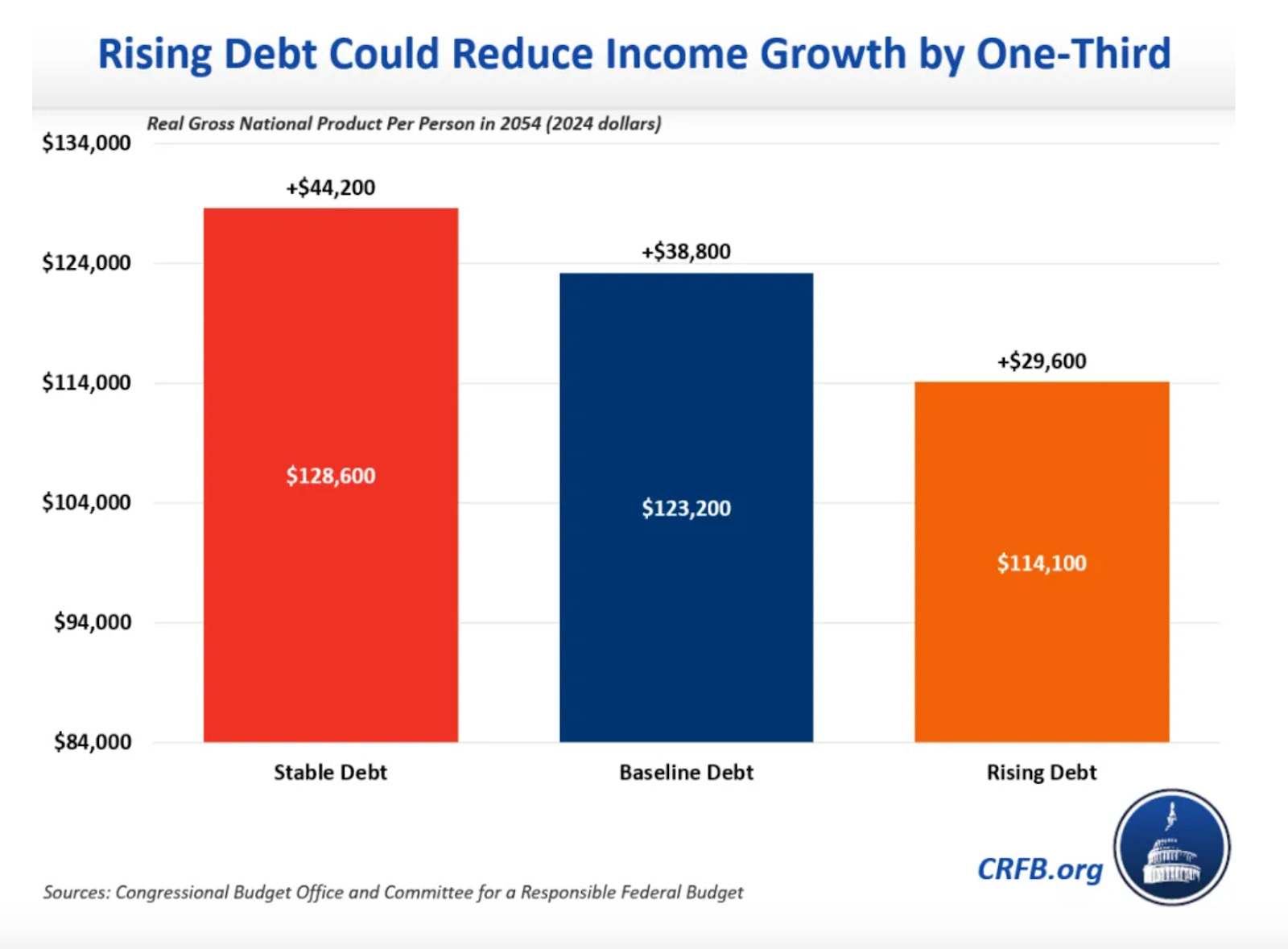

Rising debt stifles income growth. According to the Committee for a Responsible Federal Budget (CRFB), real income per person would rise from $84,000 to $128,600 between 2024 and 2054 if the national debt remains stable. However, under the Congressional Budget Office’s (CBO) current baseline, which projects the debt-to-GDP ratio increasing from 99 percent to 166 percent by 2054, per-person income would grow to only $123,200. In CBO’s alternative scenario, where the debt-to-GDP ratio rises to 294 percent in 2054, income would only increase to $114,100 - one-third less growth compared to the stable debt scenario (see the figure below). Beyond stifling income growth, an unsustainable debt raises interest rates, increasses the risk of a fiscal crisis, and limits the nation’s ability to respond to emergencies. As Dominik Lett and I have noted: “Lawmakers should adopt a concrete plan to stabilize U.S. debt as a percentage of GDP through fiscal restraint to unleash economic growth and boost American incomes before a potential fiscal crisis forces their hands.”

Will interest rates stay higher for longer? Mercatus Center’s David Beckworth and Mary Daly, president and CEO of the Federal Reserve Bank of San Francisco, discussed factors influencing R-star, the long-term equilibrium interest rate. Beckworth noted that the aging population could lower R-star, while persistent deficits may push it up. He highlighted the uncertainty around the effects of artificial intelligence (AI), which could raise R-star through productivity growth or lower it by increasing life expectancy, leading to higher savings and thus, lower rates. Daly emphasized the global nature of R-star, highlighting the significance of considering the same factors in other countries as well. Despite the uncertainties around long-term interest rates, as Lett and I have pointed out, “Congress should proactively pursue fiscal reforms” that “would also signal to markets that Congress is serious about tackling the long-term debt challenge, strengthening the norms that underlie the credibility of US Treasuries.”

Social Security pays excessive benefits to the wealthy. Peter Coy, a writer for The New York Times, argues for lowering Social Security benefits for wealthier beneficiaries while increasing them for lower-income individuals. Coy writes: “One reason that Social Security didn’t provide more of a safety net to lower-income people when it was enacted in 1935 is that many Southern Democrats thought Black people wouldn’t work if they had a good retirement benefit from the government [...] That racist rationale shouldn’t continue to affect the design of the program.” As I have written before, “Reducing benefits for higher income earners to keep program costs in check, and especially as part of a more fundamental rethinking [transitioning to a flat-benefit system] of the proper purpose of an old-age-income support program, is a better alternative than raising taxes on current workers.” This approach would better protect seniors from old-age poverty without providing excessive benefits to wealthy retirees.

“Deficits” reduce growth. Or better, expenditures with NPV <0 reduce growth