Debt Digest | Rethinking Social Security: New Paper Release

Links & Fiscal Facts

Today, we released a new Cato policy analysis, “Rethinking Social Security from a Global Perspective,” which explores Social Security’s structural problems and draws lessons from pension reform experiences in Canada, Germany, New Zealand, and Sweden. This paper provides a high-level summary of our upcoming book, Reimagining Social Security: Global Lessons for Retirement Policy Changes, to be published in August 2025.

See the paper’s summary blog here.

Here are this week’s reading links and fiscal facts:

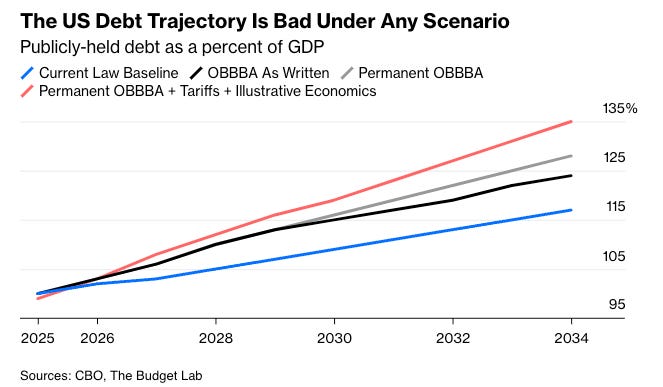

The US debt could hit 135 percent of GDP by 2034. Ernie Tedeschi, director of economics at the Budget Lab at Yale University, analyzes the GOP reconciliation bill’s impact on the debt trajectory by incorporating three realistic assumptions not included in conventional scoring. First, as history shows, temporary provisions—such as no tax on tips—are likely to be made permanent. Second, tariffs and anti-immigration policies will slow productivity and labor supply growth. Third, if interest rates stay at today’s levels, debt servicing costs will outpace the Congressional Budget Office’s (CBO) estimates, which assume lower rates over the next decade. Tedeschi writes: “Take these three risks together and debt becomes even more catastrophic, rising to 135% of GDP in 2034 rather than 117% under current law [see figure below].” Notably, as the figure shows, the US debt trajectory is unsustainable under any scenario related to the GOP bill. Tedeschi concludes: “Congress still has time to make the tax and spending legislation more fiscally responsible, but the window is closing. The question is whether lawmakers will choose short-term political gain over long-term economic stability.”

Economic growth won’t stabilize debt. Mercatus Center’s Tyler Cowen summarizes a recent paper by Douglas Elmendorf, Glenn Hubbard, and Zachary Liscow, which assesses whether economic growth can meaningfully reduce budget deficits. “To stabilize the debt-to-GDP ratio through productivity growth, we’d need to grow at an unrealistically fast rate,” writes Cowen, noting that the paper doesn’t account for the GOP reconciliation bill, which would further increase deficits and require even faster growth. The authors find that pro-growth policies in areas like immigration, housing, and R&D wouldn’t increase productivity growth at a sufficient rate to offset their budgetary costs and significantly reduce deficits. However, some policies, like increasing immigration of high-skilled workers and easing housing restrictions, would improve the debt trajectory. The paper also finds that tax cuts rarely pay for themselves. That’s why Congress should ensure tax cuts are at least deficit-neutral and pair them with spending reductions to free up resources for economic growth.

A fiscal and monetary playbook for fighting inflation. John H. Cochrane, an adjunct scholar at the Cato Institute, offers guidance to the Fed and the rest of the government on how to fight the next stagflationary supply shock—for example, caused by tariffs and the trade war. Cochrane recommends the Fed exercise its independence and “say no to buying trillions of Treasury debt, to holding down interest rates, to financing Treasury handouts, [or] to lower rates in order to weaken the dollar.” On fiscal policy, he warns against Covid-like stimulus spending and calls for spending “wisely.” He emphasizes the importance of restoring fiscal space to reassure investors that future borrowing will be repaid from tax revenues or spending cuts, avoiding driving up interest rates. Lastly, Cochrane recommends that the Treasury “borrow long” to be insulated from Fed interest rate hikes.

The current fiscal path may end with the Fed monetizing the debt. Willem Buiter, a former member of the Monetary Policy Committee of the Bank of England, and Anne Sibert, a professor emerita of economics at Birkbeck, University of London, argue that fiscal dominance is increasingly likely. “[The Fed] will do whatever is necessary to prevent a sovereign default, because the Fed’s financial-stability mandate (the Financial Stability Act of 2010 mentions the Fed 179 times) undoubtedly trumps its monetary-policy mandate of maintaining maximum employment, stable prices, and moderate long-term interest rates,” they write. Buiter and Sibert add that the Fed cannot credibly threaten to withhold debt monetization to pressure Congress into fiscal responsibility, and conclude: “Thus, the Fed will have no choice but to engage in sovereign debt purchases that it knows to be incompatible with its monetary-policy objectives.” Read more in this blog by Boccia and Dominik Lett on the threat of fiscal dominance.

Cato’s Vision for Liberty. In 2022, the Cato Institute launched the Vision for Liberty Campaign—”to expand our impact and accelerate the spread of the ideas that drive human flourishing,” through producing independent research, educating future leaders in liberty, and improving digital engagement in a fragmented media environment.

In the campaign video below, Boccia underscores why 2025 is a crucial year for fiscal reform:

“2025 is a pivotal year for fiscal policy. There’s a lot of potential with this administration and its desire to cut spending and red tape. Cato has the intellectual firepower—without the political bias—to really advance those good ideas at these pivotal moments.”

We’re deeply grateful to the generous Cato sponsors across the country. Your support makes our work possible.

Read the full campaign document here. To learn more about the benefits of Cato sponsorship, click here.