Should Social Security Be Means-Tested? Lessons from Australia and New Zealand

A guest post by Michael Littlewood

This is a guest post by Michael Littlewood.

Taxpayers shouldn’t pay a pension to someone who doesn’t need it. Said quickly, that sounds sensible. Why collect tax from producers and employees and deliver a pension to someone who, on any reasonable measure, doesn’t need it?

That question is no longer hypothetical in the United States. Some analysts have proposed means-testing Social Security benefits, particularly as concerns grow about the program’s long-term finances. Mark Warshawsky with the American Enterprise Institute, for example, has proposed applying an asset test to Social Security benefits, modelled in part after the Australian ‘Age Pension,’ once the Trust Fund is exhausted.

I used to think age-related retirement pensions shouldn’t go to rich, old people who probably wouldn’t miss the pension if they no longer received it.

If that’s the starting point, we face two immediate questions: At what level of income or assets do we begin reducing the pension, and at what point does it disappear entirely? The answer depends on the chosen ‘taper rate’ — how quickly the pension is withdrawn as income or assets rise.

I come from New Zealand where our age pension (‘New Zealand Superannuation’) is a flat-rate, universal, taxable pension. It is paid to everyone above the ‘state pension age’ (65) who satisfies the residency requirements, without regard to the recipient’s ‘other’ income or assets.

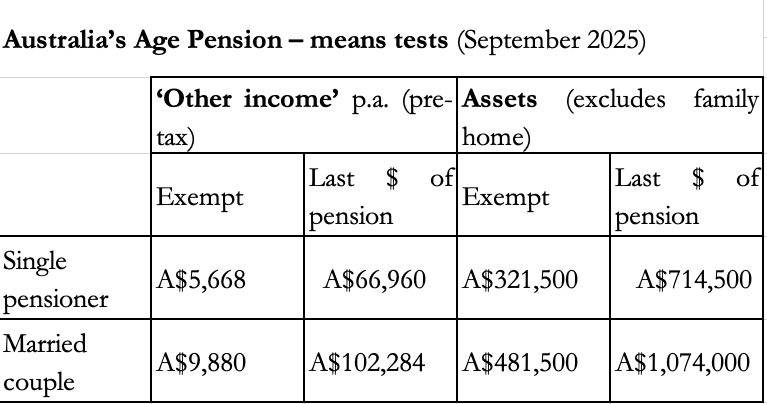

We live next door to a country (Australia) where the ‘Age Pension’ is paid in full to everyone over age 67 but only if their assets and income are below nationally set thresholds (see the appendix for a table showing the current dollar thresholds). In other words, the Age Pension is means-tested and could stop entirely if income is above a certain level or if assets exceed a certain amount (the test that sees the higher reduction in the state pension applies).

Our two countries’ retirement arrangements are similar in many ways (means-tests aside) and allow a useful comparison.

There is no doubt which is the simpler system. Any pension policy that involves understanding what each pensioner earns or owns (or earns and owns) necessarily involves intrusive, regular inquiry and regulation and Australia illustrates that perfectly. Assets and ‘other’ income are measured twice a year, and the Age Pension is adjusted accordingly[1].

In this business, simplicity is a virtue.

People adapt to the rules. Back in the 2000s, when New Zealand had some decent data, I ran a comparison, using longitudinal studies of household finances in our two countries. In Household wealth in Australia and New Zealand[2], I analysed all households’ holdings in 2006, by asset class. That comparison showed that, as might be expected, the public policy rules significantly affected the make-up of average household assets between the two countries.

I grouped the assets to see what proportion of assets households could access/sell to support their retirement incomes. The 2006 answer, across all households, was that Australians had 50.5% of total net assets available to support their post-retirement needs; New Zealanders had 49.4%. Not so different despite the differences in public policy.

Updated data from New Zealand would be welcome. But absent major changes in policy design, there is little reason to expect significant shifts in asset patterns, either within New Zealand or relative to Australia.

Australia’s combination of compulsory saving and means-testing of the Age Pension also changed other behavior. It seemed to contribute to their ‘retiring’ earlier than New Zealanders, acquiring greater debt in the years leading up to retirement, working less than New Zealanders after the state pension age and, possibly, over-saving for retirement[3].

Some think that the US Social Security pension should be means-tested. For example, Mark Warshawsky[4] suggests an asset test rather than one based on income and assets (as in Australia) or just income. He argues that net worth is a better measure of welfare and, unlike income tests, doesn’t ‘over tax’ labor earnings. He proposes that, for beneficiaries aged 62-74, Social Security should be reduced by $78 for each $1,000 of assets over $313,625 (2020 dollars). He calculates that 45% of affected beneficiaries would receive full benefits, 16.1% reduced benefits and 38.9% would see their benefits fully eliminated.

To be fair, Warshawsky sees this as a stop gap to apply when the Social Security Trust Fund ‘runs out’ but then wonders whether the policy could continue, if necessary. However, his is a cost-driven suggestion, rather than one driven by benefit design principles. For starters, as Warshawsky himself acknowledges, “… a net worth means test applying to millions of beneficiaries will be challenging to administer.”

Based on our antipodean experience, means-tests tend to provoke avoidance activities that aim to limit the impact of the asset- or income-test on net incomes in retirement. Australia shows how the personal financial planning industry is based, in part, on means-test avoidance[5].

A better way to develop retirement income policy is to design the ‘best’ scheme from first principles and only consider cost as a second-order consideration. Is the Social Security pension the best it can be, cost to one side? I suggest it isn’t.

Policymakers should hit pause on means-tests for Social Security. From this distance, they don’t have sufficient data to make informed decisions. A longitudinal study of households’ finances is the only satisfactory way to gather that. For example, who can say that the present pension is fit for purpose without understanding how households save privately over time, decide when and how to retire and manage financially during their retirement?

I myself support a fully universal, non-contributory pension, taxed as ordinary income and paid to all who satisfy residency tests, but without regard for ‘other’ income and assets. Treating the pension as ‘ordinary’ taxable income is a form of means-test, but only modestly so. NZ’s top personal tax-rate is 39% - at least 61% of the pension will remain. By contrast, the objective of a means-test, such as Warshawsky proposes or as Australia applies, is to effectively tax the pension away completely. In a progressive tax system, that isn’t the point of treating the pension as ‘income’.

US policymakers should at least consider that as an option.

Michael Littlewood is an Honorary Academic at the University of Auckland and Principal Editor of www.PensionReforms.com.

Appendix

Notes:

1. The asset test for a non-homeowner is more generous: assets below A$579,500 are exempt; no pension is paid for assets of more than $972,500.

2. For comparison purposes, the median wage in Australia was A$74,672 a year (US$48,074) in May 2025 (see here).

[1] Australian authorities require information from each pensioner on a regular basis: see here for the assets test and here for the income test. There is even a ‘deemed rate’ of return on financial assets for the income test, regardless of the return actually earned (see here). Centrelink is the agency responsible for implementing the tests in Australia. Its website lists eight different kinds of income (including some deemed income) and nine different types of assets that have to be considered twice a year. The thresholds (asset limits and cut-off points) are reviewed three times a year. The potential for bureaucratic mistakes is significant.

[2] RPRC PensionBriefing 2015-5 (2011) accessible here.

[3] See, for example, Money in Retirement – More Than Enough (2018) by Brendan Coates and John Daley, Grattan Institute (accessible here). The authors argue that Australians are already saving too much for retirement so that even the latest move to a 12% contribution rate in 2025 will probably result in a misallocation of resources.

[4] What Happens When the Social Security Trust Fund Is Exhausted: An Alternative Contingency Policy, AEI Economics Working Paper 2026-05 (accessible here).

[5] See for example The Age Pension Means Tests: Contorting Australian Retirement, Anthony Asher and John De Ravin (2020), a book chapter accessible here. The authors conclude: “Means tests….also provide very strong incentives for pre-retirees to engage in a range of strategies to maximise their age pension. Apart from the unnecessary fiscal burden that such strategies impose on taxpayers, they also distort savings and consumption decisions and asset prices (especially of the principal residence) and cry out for change.”