Fiscal Illusion and Deficit Spending

“Budgets cannot be left adrift in the sea of democratic politics.”

Americans are under a fiscal illusion. High and persistent deficits and debt pass a large share of the cost of government spending to future generations. This leads to greater demand for government than if taxpayers were internalizing the full cost today.

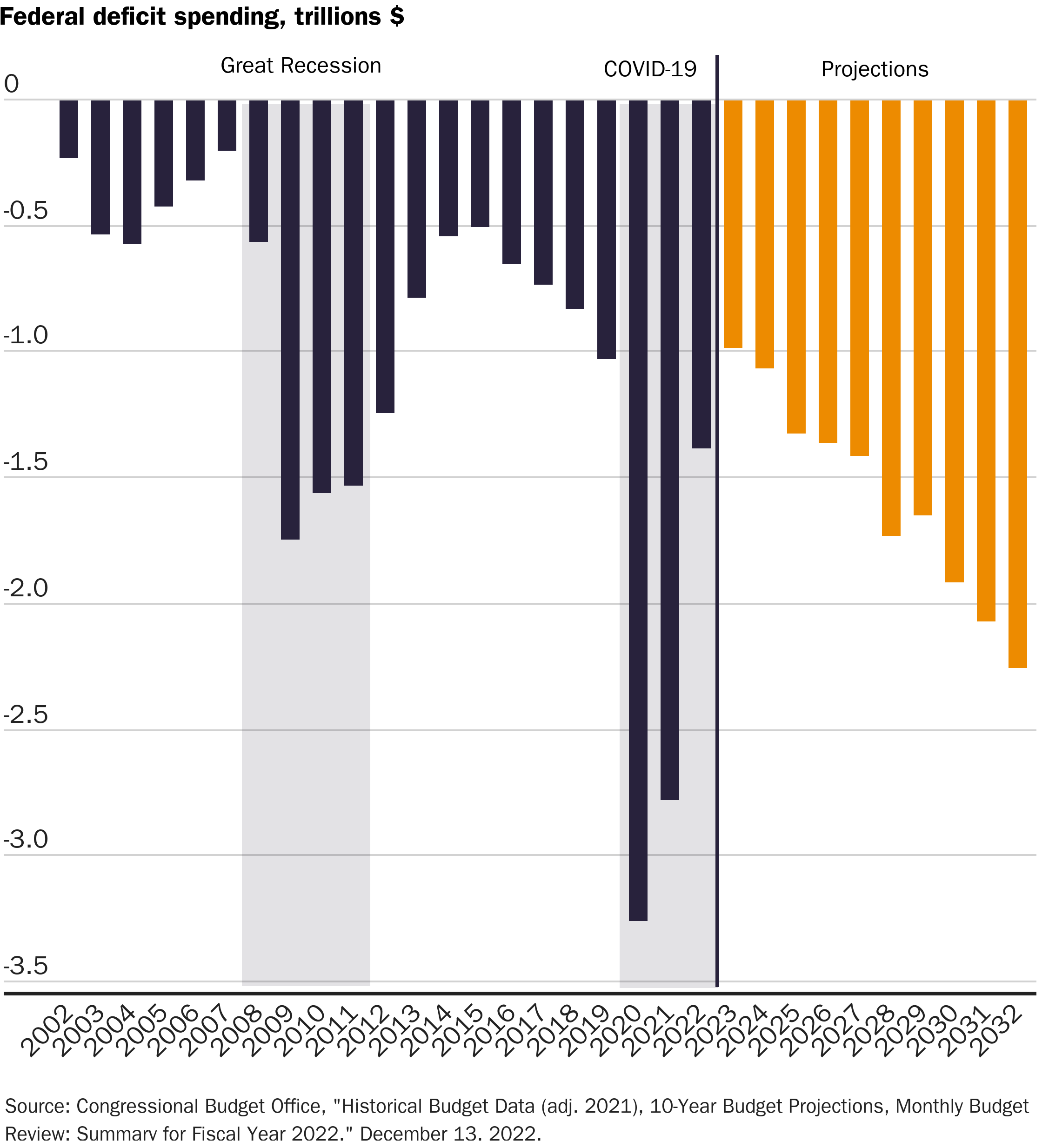

According to the Congressional Budget Office (CBO), the annual federal deficit is projected to total roughly $1.6 trillion over the next 10 years. That’s the amount by which federal spending will exceed tax revenue, on average, each year. These deficits will grow the federal debt held by the public to 110 percent of gross domestic product (GDP) by 2032, bringing publicly held debt to its highest level ever by the end of this decade. And this assumes no major unexpected crises or large new spending programs will drive debt to such elevated levels even sooner.

By comparison, annual deficits over the preceding two decades averaged $875 billion from 2003 to 2012 and $1.25 trillion a year from 2013 to 2022 (adjusted for inflation). These periods were also characterized by major crises. During the decade from 2002 to 2011, the U.S. experienced the Great Recession—the most severe economic crisis in the U.S. since the 1930s. The last decade will be remembered for a 100-year pandemic, during which entire economies mostly shut down to reduce the spread of COVID.

This raises the question: why are deficits projected to be so high and persistent into the next decade, even after the pandemic emergency has ended and without CBO projecting a new crisis?

Democracies tend toward perpetual deficits. Politicians gain the favor of their constituents by delivering tangible benefits such as transfer payments and government services. Some programs are broadly popular such as Medicare and Social Security. Even so, they are likely larger than they would otherwise be, were it not for fiscal illusion. In other instances, special interests will coalesce to exert pressure on elected officials to support policies that benefit them, even if those policies are not in the best interest of the broader public. This leads to the adoption of policies that provide benefits to a small number of individuals or organizations at a dispersed cost to taxpayers who have far fewer incentives to organize to protect themselves.

Deficits are a way to meet current constituent demands without imposing the associated costs on them.

This explains why we’ve seen major entitlement expansions over recent decades and why earmarks are so popular among members of Congress. As I’ve written previously, “while inflation‐adjusted defense spending has remained relatively flat, nondefense spending on entitlements and other social and economic programs, has expanded significantly.” However, paying for such initiatives with additional taxes or spending cuts in other areas could prove unpopular with current voters. It thus seems politically easier to finance government expansions with deficits. Deficits are a way to meet current constituent demands without imposing the associated costs on them.

The late Nobel laureate and economist James M. Buchanan wrote extensively on fiscal illusion in his work on public choice theory. Fiscal illusion arises when the true costs of public policies are obscured or hidden from view, leading individuals to underestimate the policies’ impact. Government programs appear less costly to taxpayers than they are because the current generation bears only part of the burden. Deficit-financing transfers some of the burden to future generations in the form of government debt obligations. This fiscal illusion leads current taxpayers to demand more government than they otherwise would and harms future taxpayers in the process.

Current taxpayers do incur some of the cost today via a relatively less efficient distribution of scarce resources that would otherwise go to more productive non-political uses. Fiscal illusion also contributes to the inefficient allocation of resources, including the overconsumption of certain goods or services, and underinvestment in others, leading to a less efficient and productive economy. In that way, current taxpayers pay some of the cost of current deficits.

Fiscal illusions can take numerous forms, and my Cato colleague Chris Edwards previously summarized nine common techniques, including uneven taxation, inflation, and regulation.

Buchanan argued that taxpayers suffer from fiscal illusion. Transparent taxation can help constituents better internalize the costs of government spending, enabling more appropriate trade-off calculations that weigh benefits against costs. Shifting a large share of those costs to future generations by deficit-financing camouflages the opportunity cost of spending today and thereby undermines effective cost-benefit analysis by taxpayers.

“Budgets cannot be left adrift in the sea of democratic politics.”

Buchanan’s insights regarding the democratic tendency to incur unsustainable deficits and debt led him to the conclusion that “restoration [of the balanced budget norm] will require a constitutional rule” that is both “legally as well as morally” enforced. We need rules that bind lawmakers to limit the propensity of government to expand and to protect future generations who aren’t yet taxpayers. As Buchanan and George Mason University economist Richard Wagner wrote in Democracy in Deficit, “Budgets cannot be left adrift in the sea of democratic politics.”

Are the American people and their legislators motivated to correct the unsustainable deficit spending that characterizes current U.S. budget policy? Or will it take a fiscal crisis to force a correction? It remains to be seen. The most recent fiscal restraint enacted by members of Congress as part of a debt limit increase came on the heels of a global financial crisis that birthed a political movement (the Tea Party) that demanded more responsible budget policy. The Budget Control Act of 2011 (BCA) proved inadequate, and its limited success was short-lived. The BCA also required Congress to vote on a balanced budget amendment, which failed.

Nevertheless, there is still hope. The 118th Congress will confront the federal debt limit in 2023. This is a key legislative opportunity to pursue a fiscal stabilization package that pairs the inevitable increase in the debt limit with policies that stabilize the growth in the debt. Legislators should focus on reforming entitlement programs, reducing and capping discretionary spending, and banning earmarks. They should also adopt a more transparent and effective budget process, including rules that limit the tendency of our democratic system of government to accumulate deficits. Will they?

Reading Rec’s and Fiscal Facts

Better budget rules and processes can reverse the growth in government spending and inflation. Matthew Dickerson recommends a host of quickly implementable reforms in three main areas: increasing transparency and accountability, scoring more accurately, and controlling the spending growth.

Congress spent $279 billion on improper payments in 2021. Rachel Greszler explains that “health insurance programs and child-related tax credits have the highest rates of improper payments.” To address the “longstanding and rising” trend of improper payments, she provides several reforms to “protect the integrity of taxpayers money.”

Medicare is central to fixing health care and the federal budget. James Capretta argues that “rampant waste, excessive administrative costs, and irrationally elevated prices” cause higher premiums and contribute to government borrowing. He recommends leveraging market incentives to improve beneficiaries’ choices and reduce total spending.

Hello Romina,

I read Buchanan's treatise on public debt. I even wrote an article on it. He and so many others fail to understand that all government expenditures, whether taxed or borrowed, are deficit financed.

And who pays for the expenditures of the day? Taxpayers and lenders of the day. The funds, or rather resources are consumed in the here and now, not in the there and later.

Economics and really all of science are full of silly maxims like "All Debt is Future Taxes."

Has a bank ever repaid one dime borrowed in its long history? Not a one, unless it got into some financial trouble.

Are IBM's debts greater today than they were yesterday? Absolutely.

And are the debts of governments the world over greater today than they were yesterday. Unless financially troubled, the answer is invariably yes.

Because his starting position rests on a faulty maxim, Buchanan frequently doesn't know what he's talking about. Nor do any of those relying upon his works as proof for often erroneous statements on public finance and debt.