Emergency Spending Is on the Rise: Here’s How Congress Can Stop It

$85 billion in emergency spending to hitch a ride on the omnibus

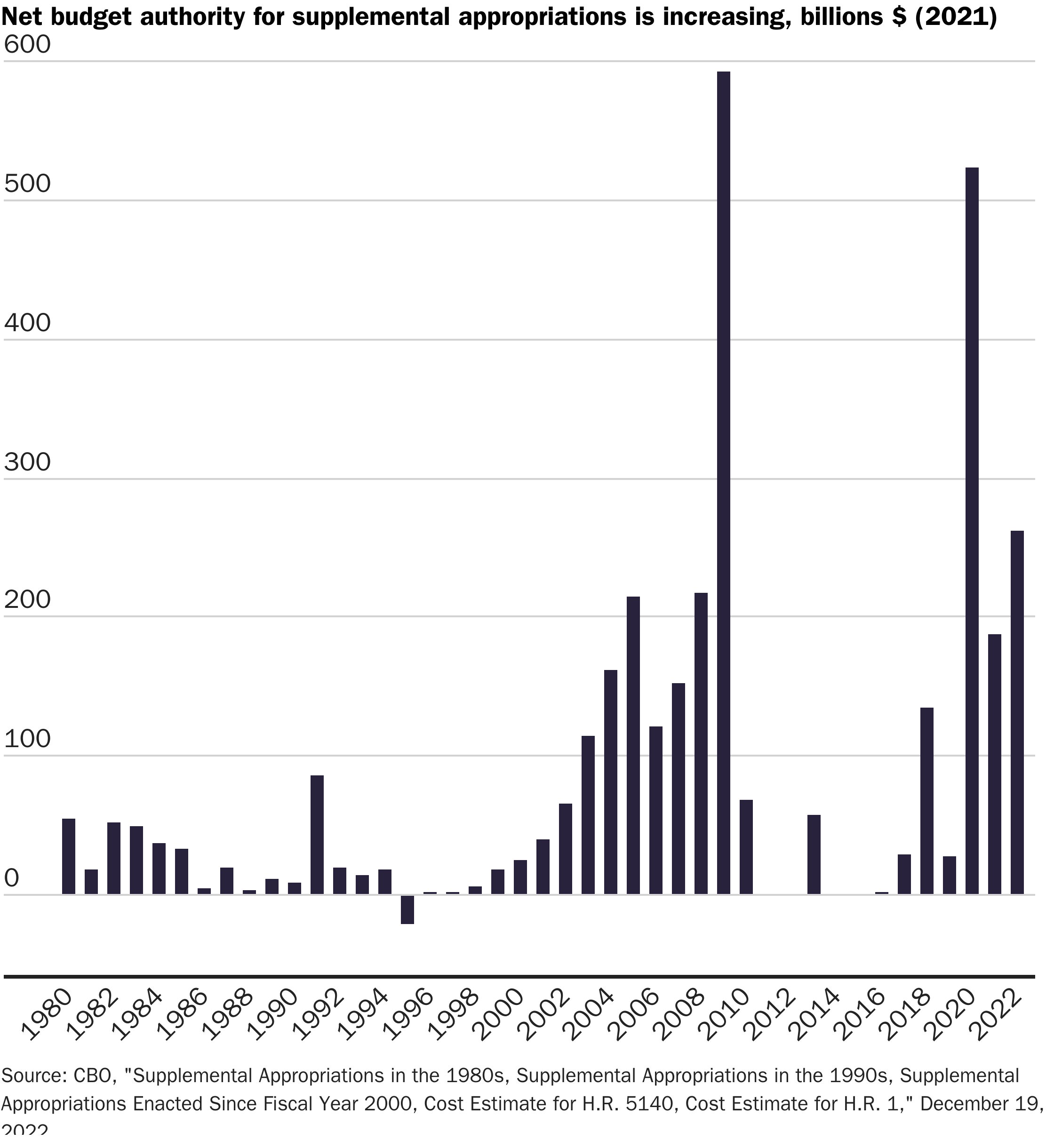

Congress has spent a combined $1 trillion through supplemental appropriations over the last five years in inflation-adjusted 2021 dollars. While most of the supplemental spending since 2020 was in response to COVID-19, supplemental appropriations are on the rise over the long term (chart below).

Reject a last-minute, lame-duck emergency supplemental that will drive up deficits and debt.

Supplemental appropriations are primarily emergency spending that falls outside of regular budgeting procedures. Congress is increasingly using crises as justifications to spend more. Now, the Biden administration has asked Congress to tack on an additional $85 billion in emergency spending to discretionary appropriations that are set to expire after December 23. Congress needs an enforceable rule requiring offsetting spending reductions to increases in supplemental spending. This would effectively limit emergency spending growth.

Most funding in supplemental appropriations is designated as emergency funding. However, what qualifies as an emergency is not well-defined. Congress has enormous latitude in determining what appropriations it designates as emergency funding. Congress is increasingly relying on supplemental appropriations to fund ongoing government priorities. Supplemental bills often include funding for projects that are neither unforeseen nor urgent. For example:

The 2013 supplemental responding to hurricane Sandy included money for improved weather forecasting which, while related to the issue of hurricanes, represented forward-looking funding that should be considered during regular appropriations. It also included money for salmon fisheries in Alaska, to fund a train service expansion into New York, and to preserve historic properties.

The Federal Emergency Management Agency (FEMA) has increasingly relied on supplementals to provide money for the Disaster Relief Fund. That account should be fully funded as part of regular appropriations based on trends in the occurrence and size of natural disasters.

Congress often appropriates so-called “no-year” funding that is available until spent. True emergency funding should respond to immediate needs, not linger in agency accounts until some future time.

Moreover, rushing funding out the door is more likely to lead to wasteful spending. The Government Accountability Office identified significant fraud, waste, and mismanagement of COVID-19 emergency funding. As Brian Riedl with the Manhattan Institute reported: “A Florida man fraudulently used a $7.2 million emergency loan to purchase a 12,579-square-foot mansion and several cars. A California couple fraudulently collected $18 million and purchased ‘three houses, diamonds, gold coins, luxury watches, expensive furniture and other valuables.’ Another man forged enough applications to collect $27 million in Paycheck Protection Program (PPP) funds.”

Track emergency funding and offset it with other spending reductions to limit abuse.

A brief history of emergency spending sheds light on more recent developments. The Budget Enforcement Act of 1990 (BEA) formalized the process for enacting emergency spending. Congress intended emergency appropriations to deal with unforeseen and urgent emergencies. If such a crisis occurred after Congress had enacted annual appropriations, emergency supplemental spending would allow for swift crisis response.

As part of the BEA, Congress also implemented caps on discretionary spending (programs for which Congress appropriates funding annually) along with a pay-as-you-go (PAYGO) requirement for mandatory spending (programs with permanent appropriations that receive irregular reviews). PAYGO requires that all new mandatory spending be offset with other mandatory spending cuts or revenue increases.

While emergency spending was functionally exempted from these controls, the expiration of the BEA in the early 2000s coincided with an explosion in the usage and size of supplemental appropriations. Some commentators argue that political polarization has also been rising rapidly since the early 2000s, which may be one reason why Congress is increasingly relying on supplemental bills to fund non-emergency priorities.

During the 2000s, Congress used supplementals to fund wars in the Middle East, rebuild after Hurricane Katrina, and stimulate the economy following the Great Recession. The resulting higher deficits and the rise of the Tea Party motivated Congress to negotiate the Budget Control Act of 2011 (BCA). The BCA imposed new limits on discretionary spending while allowing for emergency funding for natural disaster relief. The BCA therefore enabled Congress to use emergency designations as part of the regular appropriations process. While supplemental spending was temporarily curbed, emergency spending exempt from discretionary spending limits merely found another outlet in appropriations bills.

This week, Congress is considering President Biden’s request for an additional $85 billion in emergency funding as part of a possible $1.7 trillion omnibus spending package. The administration has requested $10 billion for COVID-19, $38 billion for Ukraine aid, and $37 billion to respond to natural disasters. Congress should reject a last-minute, lame-duck emergency supplemental that will drive up deficits and debt.

Legislators should instead include additional discretionary spending within agreed-upon discretionary topline spending levels and ensure additional mandatory spending will be subject to budget rules such as PAYGO. As mentioned above, including additional mandatory spending under the PAYGO rule requires it to be offset with other mandatory spending cuts or tax increases.

To limit emergency spending growth in the future, Congress should consider adopting notional emergency spending accounts to track supplemental appropriations and require future offsets. This is a promising approach that has worked in Switzerland. When a crisis arises, Swiss legislators have access to an emergency spending valve. Yet all such supplemental spending is tracked in a notional account which requires offsetting spending reductions in future years. This limits the propensity to abuse emergency spending for other priorities.

The increasing reliance on supplemental appropriations for emergencies reduces congressional oversight, evades spending limits, and avoids the trade-off considerations such rules are intended to impose, thus leading to more wasteful spending. Congress should adopt comprehensive budget controls in 2023, including establishing long-overdue limits on emergency spending.

Reading Rec’s and Fiscal Facts

Senate Appropriations Committee Chairman Patrick Leahy (D-VT) released the $1.7 trillion fiscal year 2023 omnibus appropriations bill. The bill reportedly includes $44.9 billion in emergency assistance to Ukraine and NATO allies and $40.6 billion for domestic emergencies such as “drought, hurricanes, flooding, wildfire, natural disasters and other matters.”

The Congressional Budget Office’s latest long-term Social Security projections estimate trust fund exhaustion by 2033, resulting in a 23 percent automatic benefit cut, absent congressional action. If Congress chose to raise current payroll taxes to cover the shortfall, this would require an immediate 4.9 percentage point increase, from 12.4 percent to 17.3 percent, raising the median household earners’ tax burden by about $3,500 per year. There are less burdensome changes Congress should make instead, like increasing the retirement age, focusing benefits on lower earners, and correcting a flawed cost-of-living-adjustment formula.

Remember the Biden blunder, claiming credit for Social Security’s historic 8.7% inflation adjustment? There’s been a lot of misrepresentation when it comes popular entitlement programs, like Social Security, during this past midterm election cycle. The Heritage Foundation’s Rachel Greszler highlights 7 Social Security facts the Biden administration left out when speaking with a group of Florida retirees, arguing that “the ‘reality’ Biden portrayed is misleading and undermines Social Security’s future.”

Government debt crowds out private capital and shifts risk from current to future generations. CBO’s Michael Falkenheim finds previous scholars may have underestimated the welfare costs of debt. The author explains: “Crowding out occurs because government debt absorbs private savings that could otherwise be used for private capital investment. Government debt also shifts risk from current to future generations…giving [current generations] a certain return in their retirement [while placing the] obligation associated with that certain return on future generations, although their resources to shoulder that burden are uncertain.”