Debt Digest | Trump’s $1.8 billion slush fund is unauthorized spending

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

Trump’s $1.8 billion slush fund is unauthorized spending. Alexander Bolton and Emily Brooks report in The Hill that Senate Republicans have cancelled plans to vote this week on a budget reconciliation package “amid a furious disagreement within their conference over the Trump administration’s proposal to establish a $1.8 billion compensation fund for MAGA allies.“ They explain that the package—which would also provide roughly $70 billion for immigration enforcement through 2029—has stalled “over disagreements among Republicans over how to put guardrails on the so-called anti-weaponization fund.” Cato’s Tad DeHaven and Molly Nixon emphasize the constitutional problem: “Settlements usually resolve claims between parties. This agreement, by contrast, says the [Anti-Weaponization Fund]’s corpus does not represent the value of Trump’s claims, but is based on the ‘projected valuation of future claimants’ claims. It is, in essence, the creation of a new spending program without congressional authorization.” They warn: “If this settlement stands, future presidents will have a roadmap for turning lawsuits into spending programs and political grievances into taxpayer-financed payouts. Congress should not let that happen.”

High inflation continues to decrease consumer confidence. Christopher Rugaber reports for the AP: “The Conference Board’s consumer confidence index slipped 0.7 points to 93.1 in May, the first decline after three months of gains.” Rugaber also notes that “inflation jumped to 3.8% in April, the highest in three years and far above the Federal Reserve’s 2% target,” and that “average hourly earnings, adjusted for price changes, shrank in April from a year earlier for the first time in three years.” This latest inflation episode may be due to the oil price spike from the Iran war, but the deeper cause is fiscal, as Boccia explains: “This affordability challenge is the result of fiscal excess and politicized policymaking that have raised costs while undermining confidence in the U.S. economy.” She prescribes the fix: “Sustainable affordability requires course correction. Fiscal restraint is essential. Slowing the growth of federal spending, stabilizing the debt, and restoring a credible commitment to budget discipline would ease pressure on interest rates and reduce uncertainty about future taxes and inflation.”

MBA tuition prices fall in response to new limits on federal loans to grad students. The Wall Street Journal editorial board writes: “Colleges are at long last under pressure to cut prices because last year’s tax bill limits federal loans for graduate students.” Under previously unlimited federal borrowing by graduate students, “Graduate programs became cash cows for universities, which raised prices to take advantage of the open spigot of federal loans.” Cato’s Andrew Gillen foresaw the positive development when Grad PLUS was eliminated with the OBBBA last summer. He cited several reasons for ending the program, including: “Grad PLUS was a massive drain on taxpayers,” “fueled tuition inflation in graduate programs,” and “subsidized wasteful education.” Gillen concluded, “many people see Grad PLUS as an important tool to make higher education affordable. But it has the opposite effect, making graduate education an increasingly expensive requirement that is often a millstone around society’s neck. Now that Grad PLUS is history, we say good riddance.”

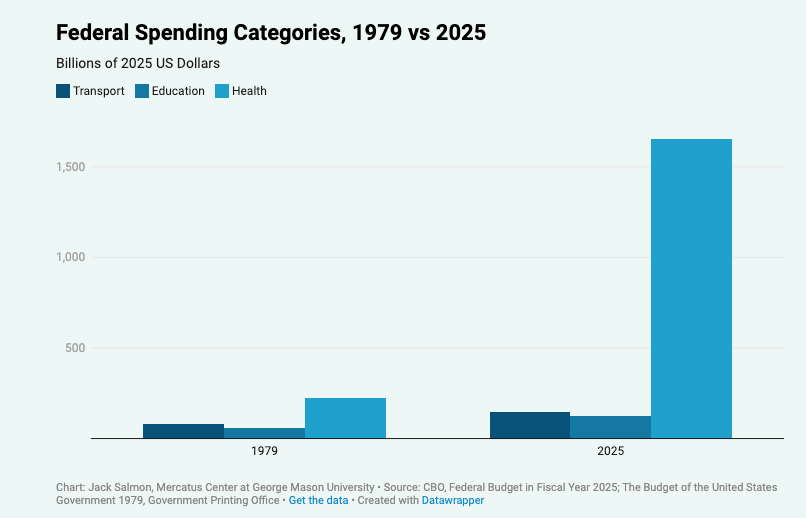

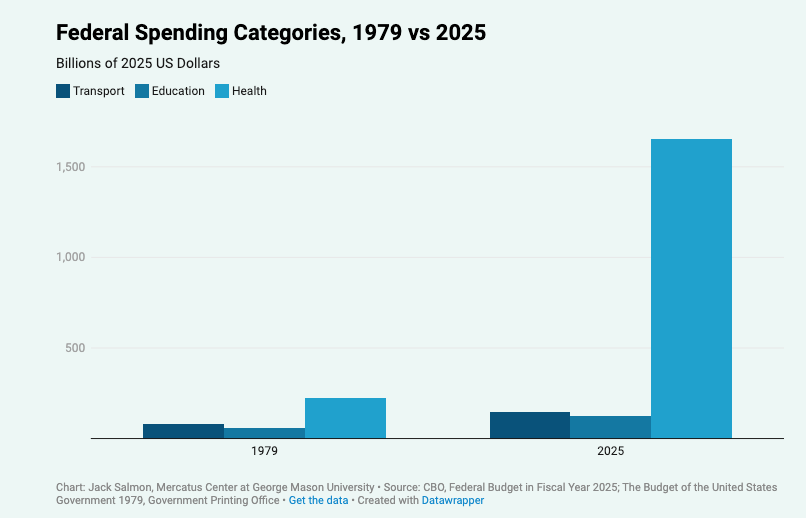

Nostalgia for the 92 percent top tax rate is completely misguided. Jack Salmon of the Mercatus Center debunks Tom Steyer’s recent claim that high historical top tax rates “built roads and bridges, expanded healthcare, and invested in education.” Salmon shows those rates raised remarkably little revenue, and that today’s wealthy actually pay higher effective rates than they did under the 92 percent top rate. On effective rates: “In 1952 when the top income tax rates were 92 percent, the top 1 percent paid an effective rate of less than 17 percent… Today, both the top 1 percent and 0.1 percent pay effective income tax rates above 26 percent.” On the spending claim: “In 1952, the federal government raised 18 percent of GDP in tax revenues. This compares with federal revenues of 17 percent of GDP today. So, relative to today, ‘all that money’ amounted to only about 1 percent of GDP in federal revenue, roughly $300 billion in today’s economy, or about 2 weeks of current government spending.” As the figure below shows, “the federal government still spends significantly more today on transportation, education, and especially on health care.”

Benefit reductions are less economically costly than tax hikes to fix Social Security’s shortfall. Andrew Biggs of the American Enterprise Institute explains how the 1977 Social Security Amendments served as a natural experiment to test how Americans respond to benefit cuts: “Economists Alexander Gelber (UCLA), Adam Isen (Treasury Department), and Jae Song (Social Security Administration), using SSA earnings data, found that, for every dollar of lost benefits, the affected Americans increased their earnings by 61 cents. Moreover, these additional earnings would be taxed by Social Security, further strengthening the program’s finances. In effect, this makes cutting benefits a ‘cheaper’ way to fix Social Security than raising taxes, because people respond in ways that also increase tax revenues.” Boccia and Nachkebia echo the argument: “reducing benefits is less economically costly than increasing younger workers’ payroll tax burdens. Higher payroll taxes increase labor costs, reduce work incentives, and displace private savings, creating a larger drag on economic growth than benefit reductions of what’s largely consumption income for a small group of wealthier retirees.”