Debt Digest | Tax Hikes Cannot Fix The National Debt

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

TrumpIRA.gov expands access to a potential $1,000 government retirement match. A new Cato news release explains President Trump’s new executive order and its implications. It directs the Treasury to launch TrumpIRA.gov which “allow[s] workers without employer plans to shop for private retirement accounts” and claim a Saver’s Match up to $1,000. The Saver’s Match was originally created by the SECURE 2.0 Act in 2022 under Biden. The potential price tag of Saver’s Match: “The Joint Committee on Taxation estimated that the current Saver’s Match would reduce federal revenues by $9.3 billion from 2028-2032.” If participation doubles “costs could exceed $20 billion in the first five years alone.” Boccia critiques the proposal: “Expanding government-backed retirement accounts may sound appealing, but it ignores how lower-income households actually save — and fails to address the real retirement crisis: Social Security’s looming insolvency. Policymakers are layering new spending commitments, with uncertain benefits for lower-income households on top of a system already facing a $28 trillion shortfall.” She points to a better solution in her recent op-ed in The Washington Post: “Tax-advantaged universal savings accounts, without withdrawal restrictions or government matching, would do much more to help these families. And all without increasing federal spending.”

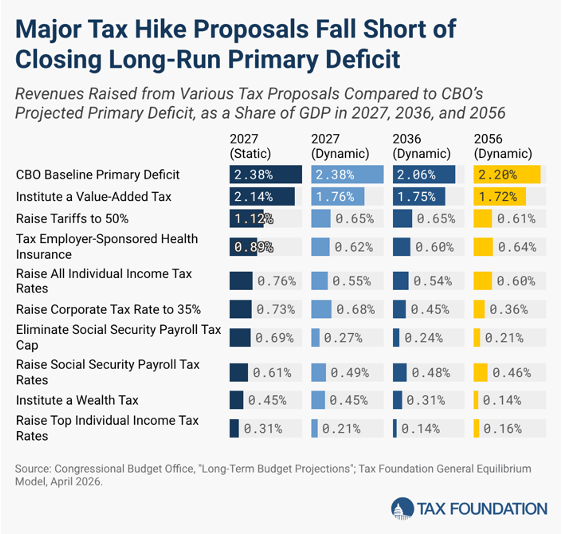

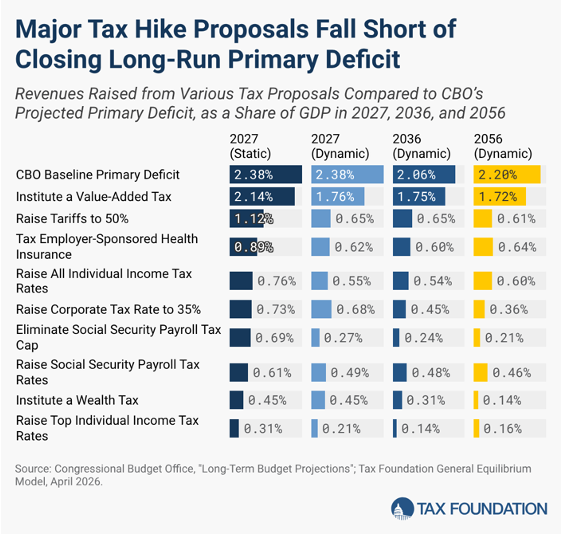

Tax hikes alone can’t fix the national debt. Tax Foundation’s William McBride simulates nine tax increases—covering individual income, corporate, payroll, consumption, wealth, and tariffs—and finds that “even tax increases large enough to close the primary deficit in the near term will lose ground over time and fail to put the debt on a sustainable course.” McBride explains why: “The most popular proposals, from hiking taxes on the rich to raising tariffs, tend to target a narrow set of taxpayers and produce the least sustainable revenues. These options are likely to introduce large economic distortions and slow economic growth without substantially improving the debt trajectory.” Cato’s Adam Michel echoes this finding: “tax-based fiscal adjustments are ‘self-defeating,’ as they tend to weaken the economy.” McBride concludes that the results “point to the need to focus primarily on reducing spending growth to reduce the debt, especially growth in the major entitlement programs.”

Trump’s tariffs undermine tax cuts from the One Big Beautiful Bill Act (OBBBA). Phil Gramm and Mike Solon argue in The Wall Street Journal that “although the government is putting money back into taxpayers’ pockets on the one hand via tax refunds, it is taking more money out via tariff-driven price increases, leaving Americans worse off financially.” They continue, “The Joint Committee on Taxation estimates that taxpayers will receive about a $188 billion reduction in federal tax liability for 2025 that they wouldn’t have received if the president’s tax cuts hadn’t become law. Those refunds and tax benefits, however, have been more than offset by the $195 billion in new tariffs collected in 2025.” Cato’s Adam Michel and Santiago Forster reach the same conclusion using Tax Policy Center estimates: tariffs amount to “a roughly $2,600-per-household tax increase in 2026 … offset[ting] a majority of the average $3,736 tax cut Americans are projected to receive in 2026 from the OBBBA.”

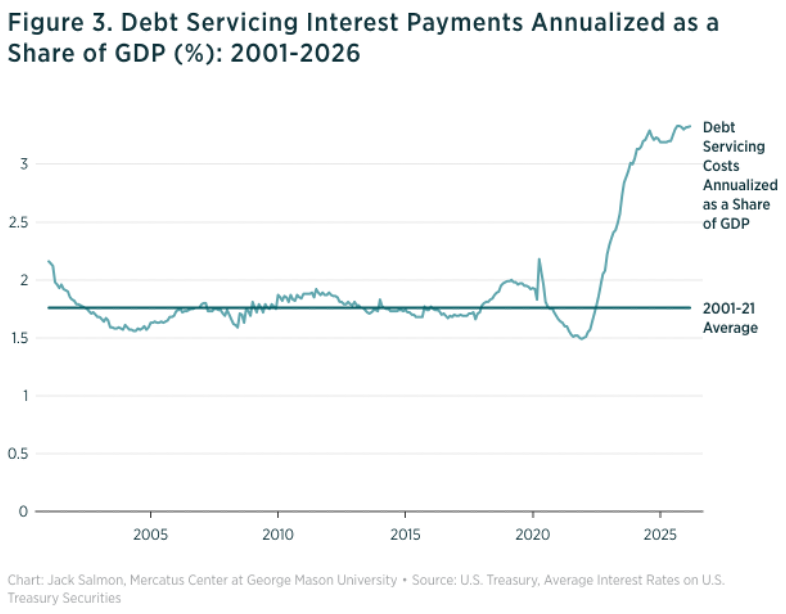

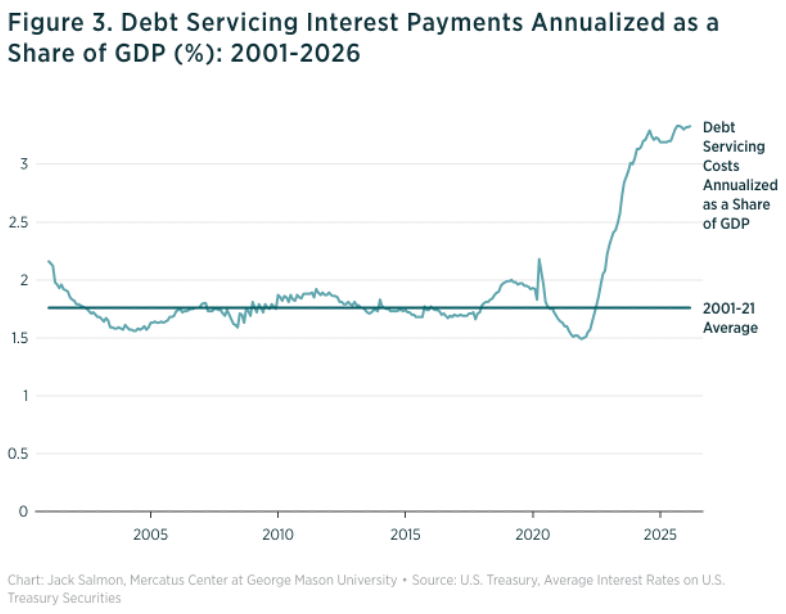

The average interest rate on U.S. government debt is nearly double its pre-pandemic norm. Mercatus’ Jack Salmon observes that “over the past 12 months, the average interest rate on U.S. government debt … has hovered around 3.3%. This rate is significantly higher than the 2000-2021 average of 1.76%.” Furthermore, “year to date, almost 21 cents of every dollar of tax revenues collected was spent on servicing the debt.” Boccia warns of the consequences: “US government debt will increasingly crowd out productivity-enhancing investments and entitlement transfers will increasingly burden younger generations with higher costs of living. America’s fiscal trajectory is on a course toward economic decline, weakening opportunity and limiting our resilience to crises.”

Downgrades of US debt are now about finances, not political dysfunction. On the Concord Coalition’s Facing the Future podcast, the American Action Forum’s Douglas Holtz-Eakin warns that earlier downgrades of US debt cited political dysfunction, but the latest one is more serious: “Moody’s just downgraded us… They said, you have too much debt and your interest takes up too much of your revenue. That’s not you can’t manage your finances. That’s your finances are a problem.” Boccia echoes the diagnosis: “The downgrade is a signal to markets—and to the public—that faith in US political institutions to manage the nation’s finances is eroding.Moody’s is essentially saying: We no longer believe you’ll course-correct in time.” Holtz-Eakin concludes, “we’re more exposed than we might have ever been in the past, so we should just get serious about controlling the growth of the debt.”