Debt Digest | Spending Drives 98 Percent of 30-Year Deficits

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

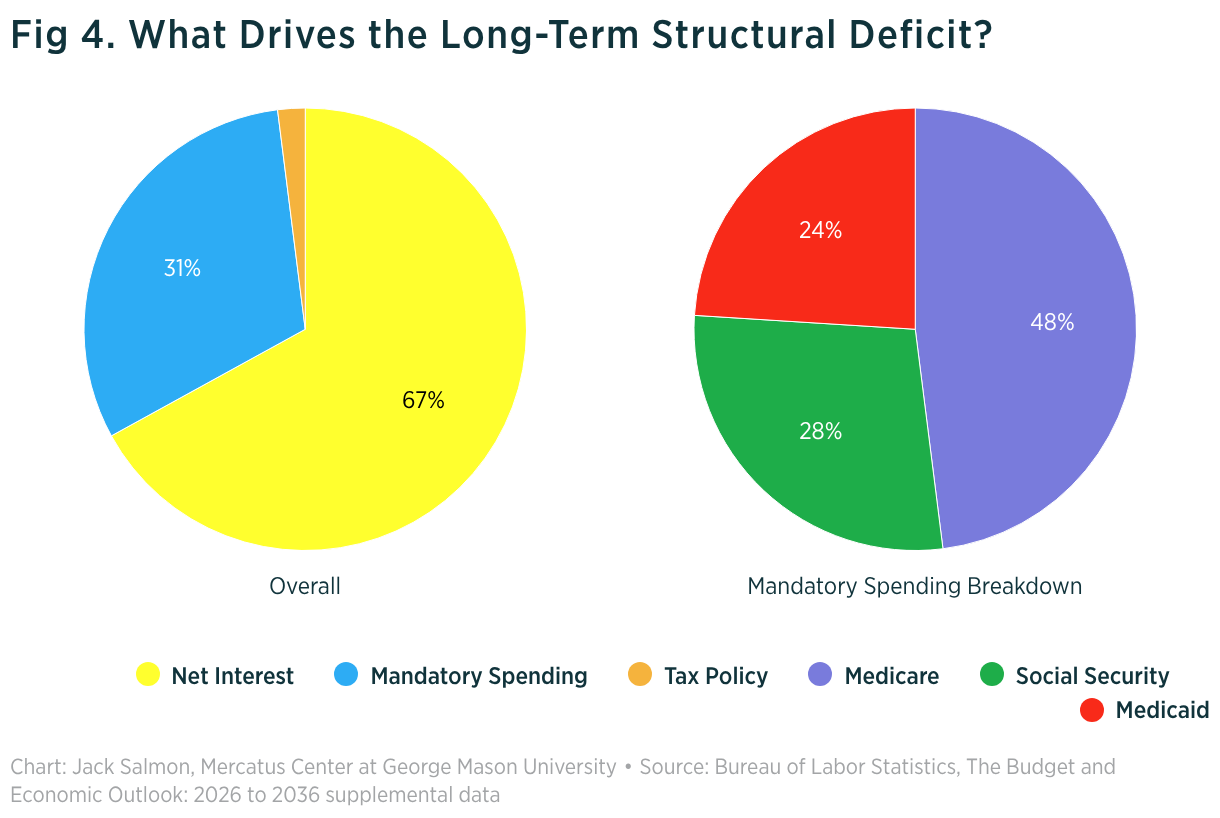

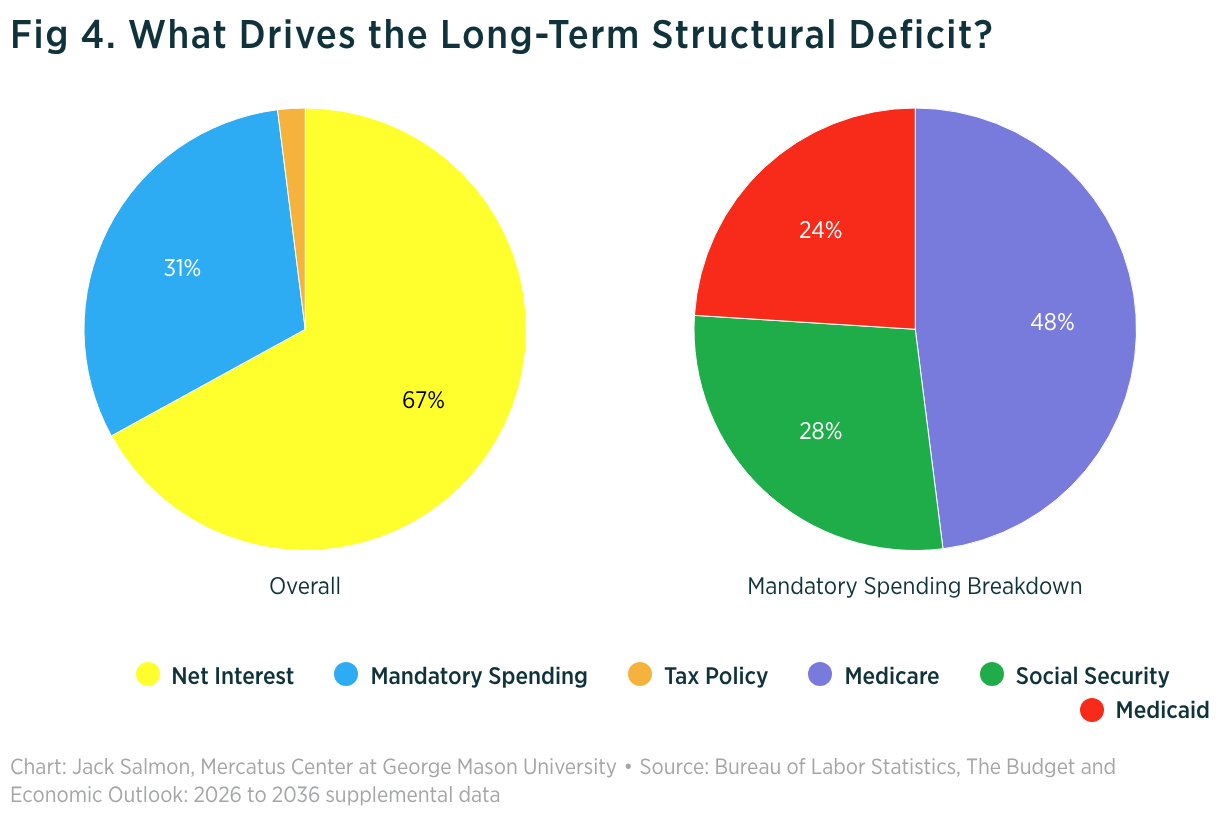

30-year deficits are overwhelmingly a spending problem. Mercatus’ Jack Salmon explains: “98% of the long-term structural deficit can be attributed to spending policy decisions, while just 2% is attributed to tax policy. Specifically, 67% of the long-term structural deficit is attributed to growth in net interest payments on the debt, while the remaining 31% is attributed to growth in mandatory spending programs.” Salmon identifies the single biggest culprit: “The entitlement program that deviates furthest from sustainable levels is Medicare, which will grow to 5.4% of GDP by 2055 (from a historical average of just 2.2%.” He concludes that “policymakers who are serious about tackling this issue will have to confront the politically difficult, but economically essential, task of slowing the growth of these programs.”

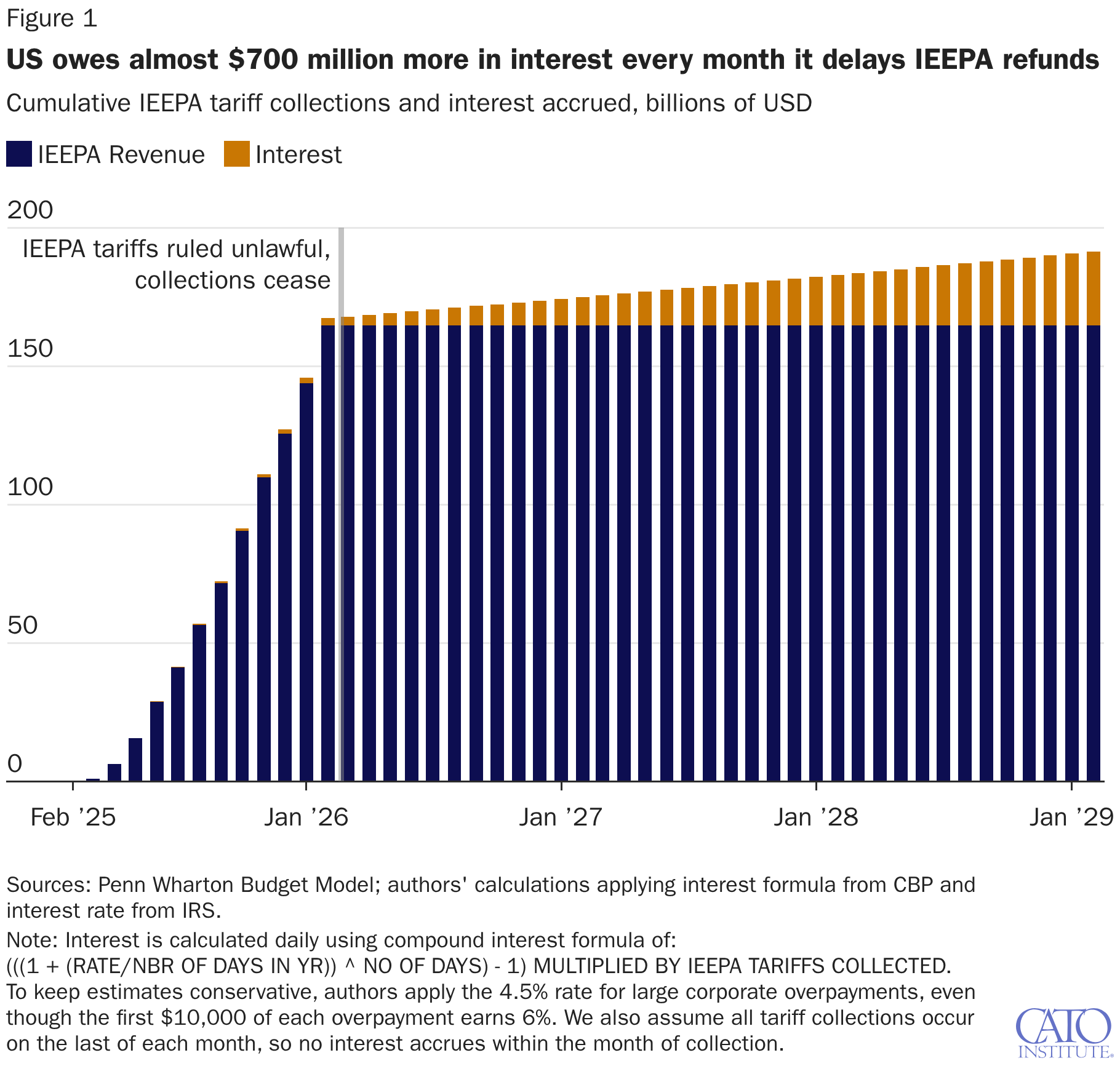

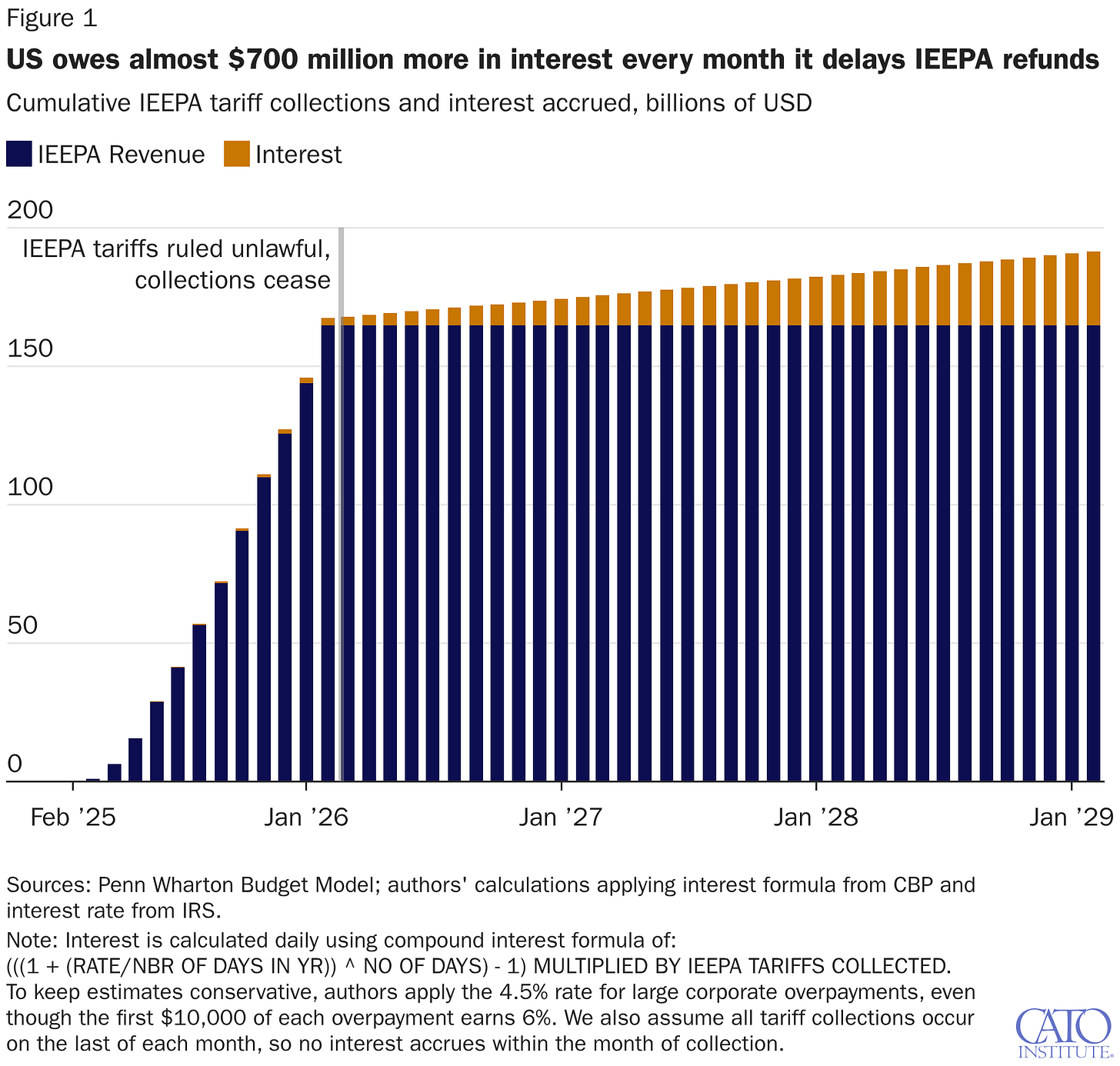

Tariff refund delays could cost taxpayers $700 million a month. After the Supreme Court invalidated IEEPA tariffs in February, Cato’s Scott Lincicome, Nathan Miller, and Alfredo Carrillo Obregon reveal the costs of “the administration’s unjustified heel-dragging […] to return the roughly $175 billion that it illegally extracted from [US importers]”. They find “that $700 million in interest is added to the final bill every month that the government delays tariff refunds, or around $23 million per day. Thus, for example, the 120-plus-day delay the government just requested would cost taxpayers almost $3 billion in additional interest. And if the government were to drag out refund lawsuits until the end of the president’s term, as he recently suggested, taxpayers would owe importers about $25 billion more. (For context, that’s almost the annual budget of NASA.)” They conclude, “Hopefully, the administration stops trying to slow down the process—if only for taxpayers’ sake.”

Wealth tax cannot work and would hurt Americans. The Washington Post writes: “Sanders wants to confiscate 5 percent of all assets every year from America’s billionaires, with the goal of stealing half their fortunes. He estimates, unrealistically, that this could raise $4.4 trillion over 10 years to fund a wish list of progressive fantasies, including something akin to a universal basic income and more government-managed health care.” The editorial highlights the problems with this proposal: a 5% tax on every asset would wipe out any gains in a normal year, force liquidation of illiquid assets, and require thousands of new bureaucrats to fight tax lawyers over valuations of wine collections, art, jewelry, and yachts. The Post points to a Cato analysis by Adam Michel: “For all the protestations about ‘fairness,’ the U.S. already has one of the most progressive tax systems in the developed world.” Michel explains that the problems of such a progressive tax extend beyond the already wealthy, as “they make each additional hour of work or investment less rewarding, weakening incentives to work longer hours, take entrepreneurial risks, start new ventures, or invest in continuing education. Over time, these effects compound, slowing economic progress and material well-being for everyone.”

Record 401(k) hardship withdrawals signal the need for universal savings accounts (USAs). Anne Tergesen reports in the Wall Street Journal: “Last year, a record 6% of workers in 401(k) plans administered by Vanguard Group took a hardship withdrawal. That is up from 4.8% in 2024 and a prepandemic average of about 2%.” The problem however is “People who take hardship withdrawals from traditional accounts must pay income tax, plus often a 10% penalty if they are younger than 59½ years old.” The recent Trump proposal of $1000 retirement match won’t address this issue, as Boccia explains, “Many low-income and younger earners don’t participate in 401(k)s because it often doesn’t make economic sense for them.” Cato’s Adam Michel shows this reality, as “43 percent of all taxes paid by taxpayers with adjusted gross income (AGI) below $5,000 went to penalties for accessing their own money.” He concludes, “Universal savings accounts fix this problem. They would give more Americans access to a savings system that protects their investments from multiple layers of tax without punishing them for needing to access their funds on their own timeline.”

End the employer-sponsored health insurance exclusion to fix healthcare affordability. Bryan Dowd and Anthony LoSasso comment on the rising premiums and unaffordability of healthcare in MedPage Today. They argue the main culprit is the tax exclusion for employer-sponsored health insurance: “Because the value of employer-sponsored health insurance premiums is excluded from workers’ taxable income, health insurance is effectively cheaper than cash wages. That encourages more generous coverage, weakens price sensitivity, and mutes competition among health plans. The result is predictable: higher spending, higher premiums, and little downstream pressure on medical providers to take responsibility for the total cost of care.” Cato’s Michael Cannon emphasizes this sentiment, “The United States will not have a consumer-centered health sector until workers control the $1.3 trillion of their earnings that the exclusion now lets employers control. Congress should act immediately to eliminate the tax exclusion for employer-sponsored health insurance. At a minimum, Congress should reduce the harms that the exclusion causes by taking serious steps to reform it. Replacing the exclusion with Large HSAs appears to be the best politically feasible option.”