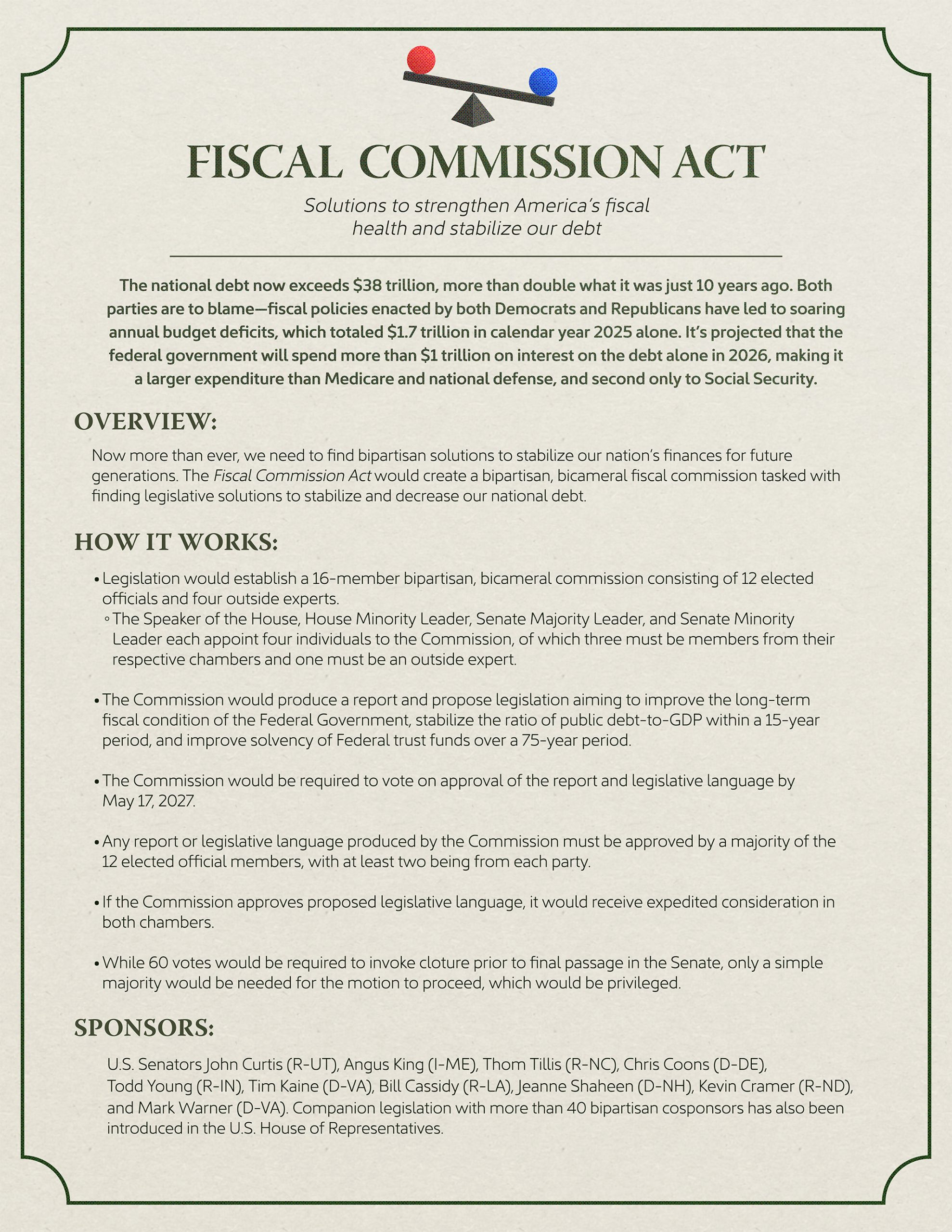

Debt Digest | Fiscal Commission Act Introduced in the Senate

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

Bipartisan Fiscal Commission Act introduced in the Senate. Senators John Curtis (R-UT) and Angus King (I-ME), joined by eight cosponsors, introduced legislation to create a 16-member bipartisan, bicameral commission tasked with stabilizing the debt-to-GDP ratio within 15 years and improving federal trust fund solvency over 75 years. Boccia comments: “I commend Senators John Curtis (R-UT) and Angus King (I-ME) for introducing the Senate companion to the bipartisan House Fiscal Commission Act, championed by Representatives Bill Huizenga (R-MI) and Scott Peters (D-CA). With interest costs on America’s debt exceeding what the government spends on national defense, as debt is on track to exceed the size of the U.S. economy next year, it is urgent that members of Congress address the growing US debt crisis, before bondholders force legislators to take far worse austerity measures or push the Fed to allow inflation to run rampant.”

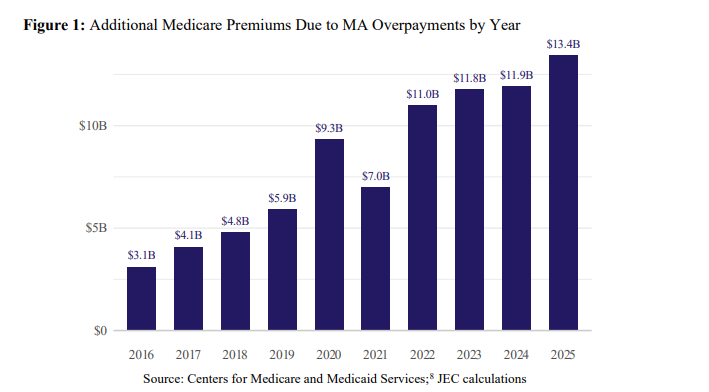

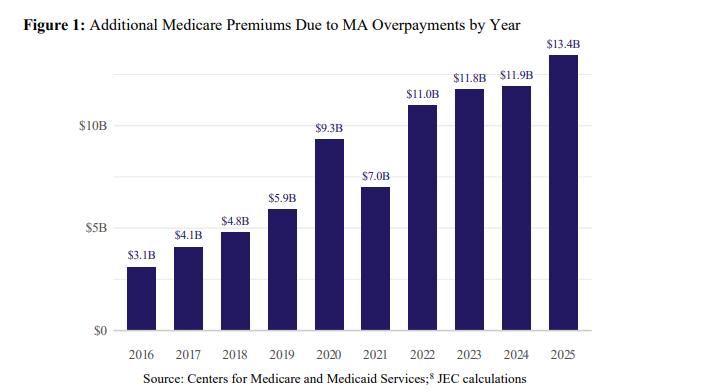

Medicare Advantage (MA) overpayments raise Medicare Part B spending and premiums. A new Joint Economic Committee issue brief reveals, “On average, covering a beneficiary in MA costs an estimated 120 percent of what it would cost in Traditional Medicare (TM). MA overpayments raise Part B spending, and because premiums are set to cover roughly one-quarter of expected costs, everyone in Part B pays more.” They continue, “MA overpayments increased Part B premiums by $212 per enrollee in 2025, totaling $13.4 billion in higher premiums. Since 2016, MA overpayments have added an estimated $82 billion to Part B premiums. TM beneficiaries, who are not enrolled in MA, bore roughly $6 billion of that burden.” As we covered in a previous Digest, the Centers for Medicare and Medicaid Services have made some progress in targeting MA overpayments, with “a net average year-over-year payment increase of 0.09% in CY 2027--far below industry expectations “between 4% and 6%.”

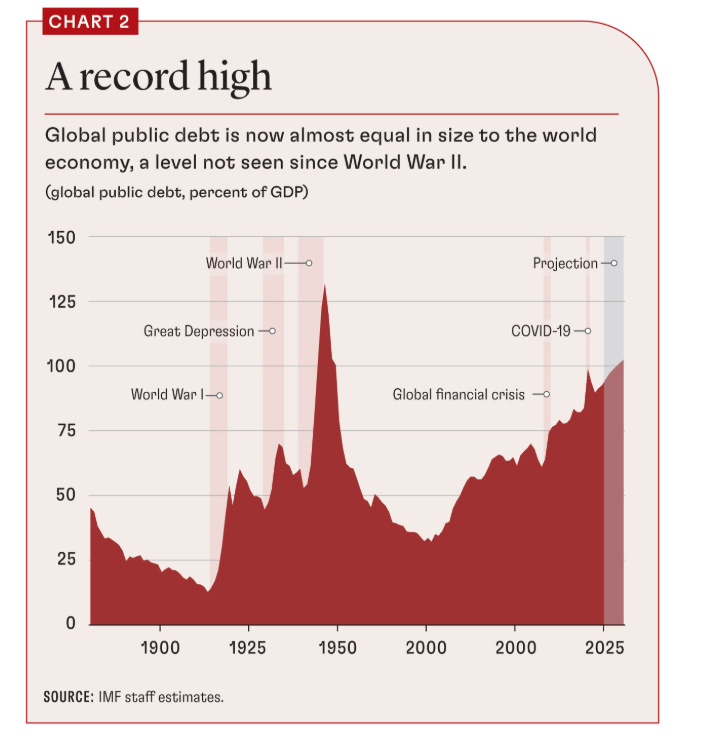

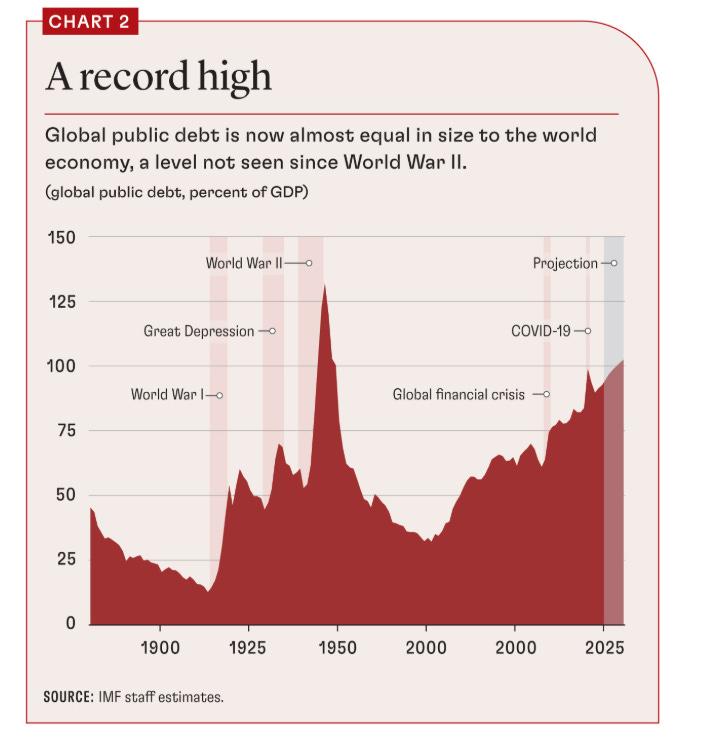

The IMF warns the era of easy fiscal choices is over, and the US is a clear example. The International Monetary Fund’s Era Dabla-Norris and Rodrigo Valdés write: “Today, policymakers face the fiscal version of long COVID—higher interest rates and rising debt costs. Global public debt climbed to 93.9 percent of GDP in 2025 and is on track to breach 100 percent by 2028—levels never seen in peacetime.” The United States is among the most indebted advanced economies, with debt held by the public at roughly 100 percent of GDP. The authors warn that high debt forecloses the options governments once relied on: “In a low-debt, low-rate world, governments could sidestep hard choices by borrowing more and hoping economic growth would generate enough additional tax revenue to service and eventually repay the debt. But today, the era of easy choices is over. Every dollar a government borrows without matching revenue implies higher taxes or lower spending in the future, at least to cover the additional interest the new debt generates.” They echo Boccia’s description of Bankruptcy—Gradually, Then Suddenly with a quote from economist Rudi Dornbusch: “crises take much longer to happen than you think, and then they happen faster than you thought they could.”

Wealth tax messaging is misleading. Adam Michel comments that “the Sanders-Khanna federal wealth tax, which the lawmakers claim would raise $4.4 trillion over a decade” is largely overstated. He continues, “Applying widely accepted estimates of behavioral responses, Kyle Pomerleau finds the tax would raise closer to $2.3 trillion, about half the lawmaker’s claim.” Michel reveals another flaw: “The Sanders-Khanna proposal would use the projected wealth-tax revenue to fund a long list of new federal programs […] What the proposal notably does not do is address the federal deficit, which is projected to rise from $2 trillion to $3 trillion per year by 2036. A decade of revenue from the proposed wealth tax would barely fund one year of the average federal deficit.” Michel concludes, “Wealth taxes and other similarly narrow tax-the-rich proposals at best obscure the true cost of expanding government. At worst, they intentionally mislead voters into believing that someone else can foot the bill for an expansive government.”

Farm subsidies keep growing, and “fiscal conservatives” keep voting for more. Cato’s Chris Edwards reveals the scale of recent farm handouts: the Trump administration passed $23 billion in trade-war bailouts in 2018–19, Congress dished out $31 billion during COVID, another $31 billion in the 2024 American Relief Act, and the OBBBA added $66 billion over ten years. Edwards elaborates, “The House GOP is currently pushing another big farm bill just months after President Trump doled out $12 billion in special farm payments. By one measure, farm subsidies are projected to soar from $23 billion in 2025 to $42 billion by 2027.” Edwards highlights the contradiction with “farm-state Republicans—they oppose ‘wasteful spending’ but are blind to some of the most wasteful programs in the federal budget.” He concludes, “If we are to tackle the $36 trillion debt, there is no better place to start than for “strong fiscal conservatives” to cut unneeded subsidies for the wealthy. The GOP stresses personal responsibility when cutting low-income welfare, and they should cut high-income farm welfare for the same reason.”