Debt Digest | Entitlement Reform is Pronatalist

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

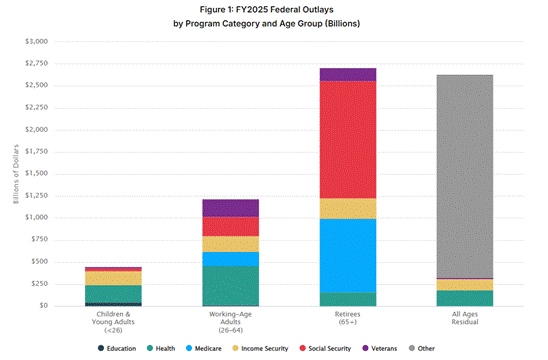

Retiree’s share of federal spending is ten times that of children and young adults. A new Penn Wharton Budget Model analysis by Kent Smetters reveals in Fiscal Year 2025, “Retirees (ages 65 and older) receive $2.7 trillion, or 62 percent of the $4.4 trillion in age-assignable federal outlays, driven mainly by Social Security and Medicare.” On a per capita basis, retirees receive $43,700 compared to $7,300 for working-age adults and $4,300 for children and young adults. This data is a perfect example of “Total Boomer Luxury Communism,” the term coined by Russ Greene which we highlighted in a previous edition of the Digest. As Greene puts it, “the essence of TBLC is that it redistributes wealth from younger families and workers to seniors, who are on average much richer.” That generational wealth transfer is no accident. As Boccia emphasizes, “rising debt is not a temporary problem. It is the result of unsustainable policy choices. Chief among them: bestowing lavish benefits on older, more politically active Americans financed by borrowing that shifts the cost to younger, less politically active generations.”

Entitlement reform may be the best pronatalist policy. Rachel Lu argues at Law & Liberty that high-subsidy family policies have failed to boost birth rates, and the real culprit is the entitlement state itself: “Elderly entitlements are the worst offenders: they socialize one of the major benefits of children while privatizing the cost. Over the longer run, entitlements also seem to erode family networks, and perhaps especially intergenerational dependence and closeness, teaching people to view the state as the presumptive caretaker instead of kith and kin.” She notes that France, Sweden, and Hungary all spend far more on family policy than the US yet have similar or lower birth rates. The cost of inaction for young workers is steep. As Boccia and Nachkebia detail, keeping Social Security solvent indefinitely could cost a median new worker $157,000 in lifetime earnings — “roughly equivalent to giving up” nearly two and a half years of pay.

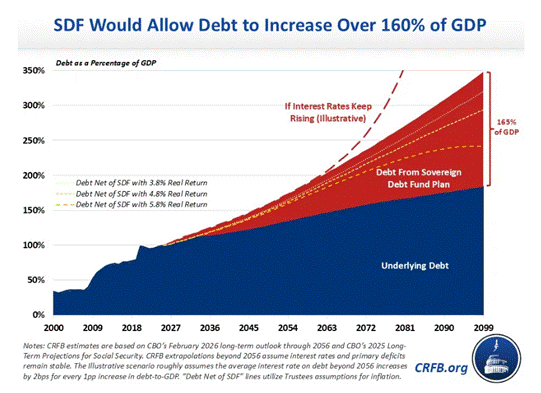

A sovereign debt fund won’t save Social Security. At a recent Senate Budget Committee hearing on Social Security’s looming insolvency, Sen. Bill Cassidy (R-LA) advocated borrowing $1.5 trillion to invest in the stock market as a backstop for the trust fund, with support from Sen. Tim Kaine (D-VA). But the Committee for a Responsible Federal Budget highlights the problems in the proposal: the plan would “add up to $170 trillion to the debt when adjusted for inflation,” “boost debt-to-GDP by at least 140%,” “expose Social Security to significant stock market risk”, “push up interest rates on government debt”, “make the government a major shareholder of private companies”, and “open the door to ‘free lunch’ budget gimmicks for future tax cuts or spending.” As Boccia and Nachkebia warn, the Cassidy-Kaine plan is “essentially a risky bet that long-run stock market returns will exceed the interest on federal debt” — and if the bet fails, taxpayers bear the loss. Worse, after 75 years the federal government would own roughly a third of the US stock market, bringing “the US economy closer to a form of state ownership — something Americans should resist.”

Weak Treasury auctions expose the risk of Fed-financed fiscal profligacy. When a recent auction of $69 billion in two-year Treasury notes drew weak demand, pushing yields to 3.9 percent, Cato’s Jai Kedia explains it exposed a flaw in the Fed’s justification for paying banks trillions in risk-free interest on reserves (IOR). The Fed claims IOR and Treasurys are fiscal equivalents, but “a two-year note carries meaningful inflation and duration risk; an overnight reserve balance does not. These are not the same instrument, and rational investors do not price them identically.” The deeper problem: “we may discover (as markets demand higher yields) that people have a limited appetite for US debt if the federal government shows no signs of ending its fiscal profligacy. As it stands, the government can simply have the Fed monetize its unending debts under the cover of IOR.” As Jeffrey Rogers Hummel explains in a guest post on the Debt Dispatch, IOR transformed money creation into another form of government borrowing — meaning “unless the Fed returns to a pre [IOR] operating framework — or Congress restores fiscal discipline — relying on money creation to finance deficits will carry far steeper inflationary consequences than it once did.”

One year after “Liberation Day,” Americans are footing the bill. A comprehensive Council on Foreign Relations retrospective marking the anniversary of Trump’s April 2, 2025 tariff announcement finds that “the average effective tariff now stands at roughly 12 percent — about five times what it was before Trump’s second term.” And according to a recent study by New York Fed economists, “Americans bore 94 percent of the tariff cost.” Cato’s Lincicome, Obregon, and Smitson also document the wreckage and conclude, “Based on the available facts, “Liberation Day” did not herald the era of economic prosperity that the president promised. Taxes, prices, uncertainty, and bureaucracy climbed, while US manufacturing, FDI, and the trade balance stood still. Exemptions proliferated; lobbying skyrocketed; and most Americans were worse off.”