Debt Digest | A Million Simulations Show That the US Debt Is on an Unsustainable Trajectory

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

Repeal the IRA energy subsidies. According to Cato’s Adam Michel, due to the energy-related provisions in the Inflation Reduction Act (IRA), energy subsidy expenditures may exceed $1.8 trillion over the next decade. He explains, “Most of the IRA tax credits are functionally similar to uncapped automatic spending programs. The cost is determined by the credit formula and taxpayer uptake.” Because of the higher uptake than projected, the subsidies could cost two or three times more than initially estimated. “Congress should repeal the IRA and the pre‐IRA energy credits. As a whole, these tax credits are a highly inefficient and expensive system of subsidizing energy from some politically popular low greenhouse gas emitting sources,” concludes Michel.

A million simulations show that the US debt is on an unsustainable trajectory. Bloomberg’s analysis, using market forecasts for future interest rates, projects the debt-to-GDP ratio could hit 123% in 2034, which is 7 percentage points more than the Congressional Budget Office’s estimate. Bloomberg also ran a million simulations, varying in variables such as GDP growth, inflation, and interest rates. 88% of them indicate that the US debt is on an unsustainable path. This outlook worsens with more realistic assumptions like the extension of most of the 2017 tax cuts. The authors concede: “Neither party favors squeezing the benefits provided by major entitlement programs. In the end, it may take a crisis — perhaps a disorderly rout in the Treasuries market triggered by sovereign US credit-rating downgrades, or a panic over the depletion of the Medicare or Social Security trust funds — to force action. That’s playing with fire.” For more on the US debt problem, see here and here.

Social Security emerged as a response to the Federal Reserve’s errors. The Laffer Center’s Brian Domitrovic explains: “Social Security came about in 1935 for one overriding reason: In the prior generation savers of money had gotten their world rocked as never before. If you retired with a nest egg in 1913, in seven years your savings got cut in half as the U.S. experienced 100% inflation. The Federal Reserve was at fault.” Nearly nine decades later, the entitlement spending-driven federal debt may lead to another Fed error. Specifically, Congress might push the Fed into monetizing the debt, a decision that can diminish private savings through inflation. As Romina Boccia and Dominik Lett recently wrote: “If Congress leaves spending corrections to the last minute, legislators may perceive the draconian fiscal consolidation necessary to bring debt under control as less desirable than monetizing the debt. In such a scenario, printing more money might become the easiest or only politically feasible way out.” For more on the threats of the Fed resorting to fiscal quantitative easing see George Selgin, The Menace of Fiscal QE.

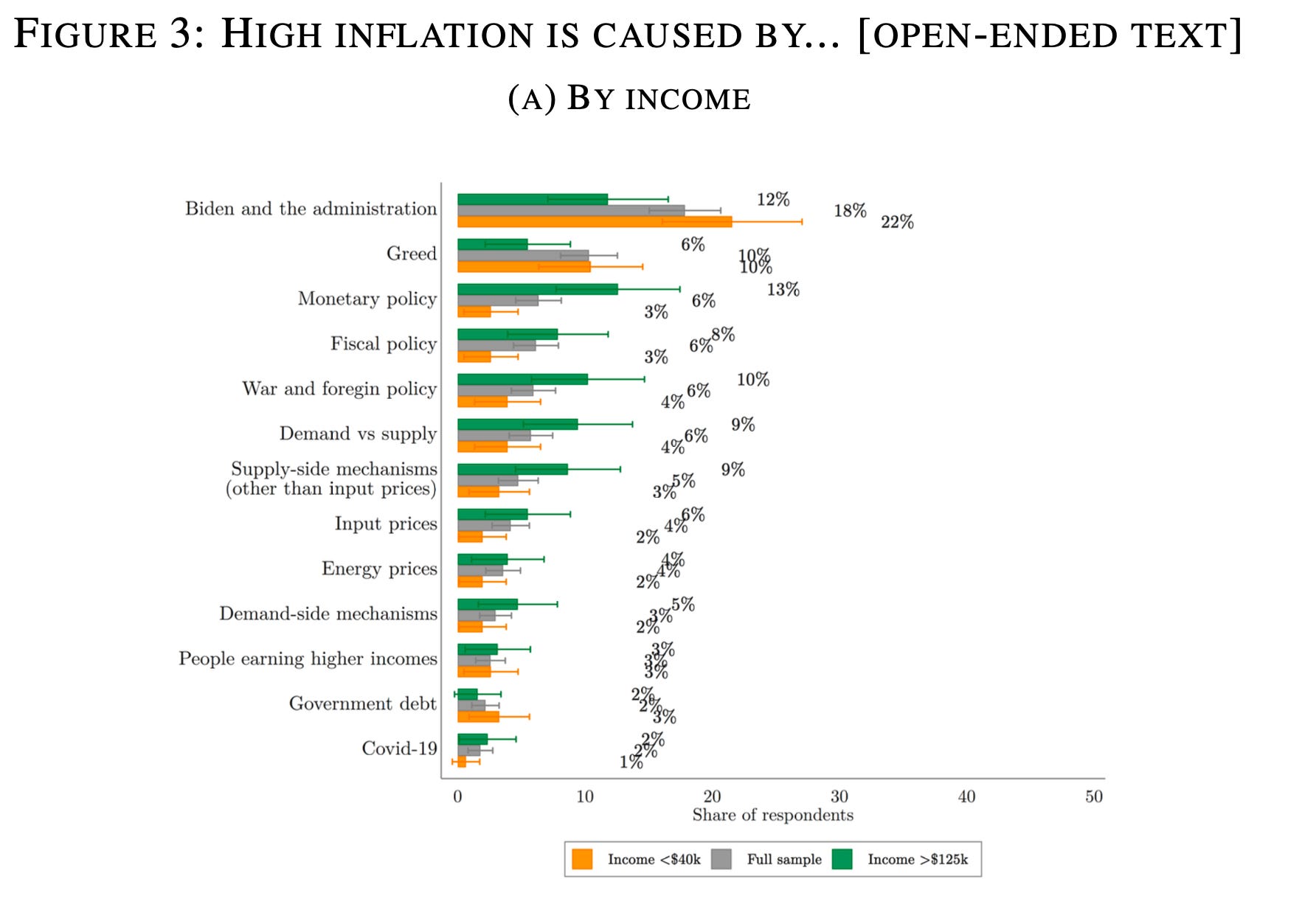

Americans really do not like inflation. A recent Harvard study, authored by Stefanie Stantcheva, illustrates the overwhelmingly negative views Americans hold about inflation. According to the study, inflation ranks first in both social and economic policy priorities among respondents. While the respondents differ in their views on the causes of inflation (see figure below), there is widespread agreement that it primarily has negative socioeconomic effects. “If there is a single and simple answer to the question “Why do we dislike inflation,” it is because many individuals feel that it systematically erodes their purchasing power,” notes Stancheva. Furthermore, inflation takes a psychological toll on individuals, with 70% of the respondents reporting that it provokes stress. For more on the causes and consequences of inflation, see here.

Automatic stabilizers to fix Social Security when Congress won’t touch it. Alicia Munnell, the Director of the Center for Retirement Research at Boston College, and William Arnone, CEO of the National Academy of Social Insurance, suggest introducing an automatic balancing mechanism to tackle Social Security insolvency. Proposing this mechanism as a response to Congressional inactivity on the issue, Munnell and Arnone write: “The key is to adopt a mechanism that automatically adjusts revenues or benefits if shortfalls emerge due to demographic and economic changes.” Kurt Couchman of Americans for Prosperity, who illustrated how this mechanism would work in detail, explains: “Automatic fiscal stabilizers would replace inaction with specific changes in statute to improve solvency and, if done well, prevent the trust funds from becoming depleted after multiple rounds of adjustments. They could also motivate Congress to act with better alternatives, but automatic enforcement must be reasonable to minimize Congress’ temptation [to] just turn them off.”