Will Economic Growth Be Short-Lived as Fiscal Challenges Abound?

Will Economic Growth Be Short-Lived as Fiscal Challenges Abound?

Lower interest rate sensitivity in the market and economic tailwinds are largely temporary, hiding the debt drag beneath the surface

The United States has been experiencing remarkable economic growth, even as debt and deficits soar to unprecedented heights. The economy has benefitted from lower interest rate sensitivity in the market and fiscal and monetary tailwinds. These dual trends are largely temporary, hiding the debt drag beneath the surface.

The economic literature is clear that high and rising government debt-to-GDP slows growth. Over time, debt crowds out more productive investments, raises interest rates, and makes America more vulnerable to crises of all types. Should Congress fail to course-correct soon, America could suffer lower growth, economy-stifling interest rates, and elevated inflation, harming current and future generations.

Stimulus-Driven Growth May Be Short-Lived

In the wake of the COVID-19 pandemic, the US has experienced impressive economic growth. In 2021, annual real GDP rocketed up by 6 percent. In 2022 and 2023, the US enjoyed roughly pre-pandemic levels of growth. For context, the US economy grew by 2.5 percent annually in the five years preceding the pandemic. Internationally, the US recovery has outpaced its economic peers. At a recent American Enterprise Institute event, Federal Debt: The Baseline and Options for Reform, chief economists from JPMorgan, Mastercard, and Apollo pointed to a few reasons why the US economy has continued to surge ahead as debt and deficits reach new heights.

First, the economy has been bolstered by strong but temporary monetary and fiscal stimulus. In response to the pandemic, Congress enacted enormous fiscal stimulus, providing direct cash transfers to consumers, generous business loans, and temporary tax relief. This was followed by a series of large spending packages, including the CHIPS and Science Act (industrial policy), Infrastructure Investment and Jobs Act, and Inflation Reduction Act (energy subsidies, health care, and tax policy). Together, these three bills will raise deficits by nearly $1 trillion over the next ten years. Add that on top of the multi-trillion-dollar pandemic stimulus, and it is no surprise that higher inflation followed.

Likewise, the Federal Reserve initially pursued a loose, expansionary monetary policy in response to the pandemic economic downturn. The Fed pushed interest rates down and conducted large-scale quantitative easing to increase the money supply and to make borrowing cheaper. Despite the Fed later tightening interest rates to combat inflation, the economy has continued to surge ahead, partly carried by earlier fiscal and financial tailwinds.

The key observation here is that most, if not all, of the fiscal and financial tailwinds outlined above are temporary. Consumers have already spent all of the savings they built up over the pandemic. COVID-era subsidies have largely run out or are ending soon. Spending from bills with longer horizons, such as the CHIPS Act and the infrastructure bill, will wane over time, as will the associated temporary deficit-fueled economic stimulus, while taxpayers will be saddled with permanently higher debt costs.

Second, lower interest rate sensitivity from many consumers and businesses has played a major role in limiting the deleterious effects of a high debt and deficit environment that’s pushing up rates. On the consumer side, around 70 percent of household debt is held as housing or mortgage debt, with 15- and 30-year fixed mortgages insulated from interest rate fluctuations. Likewise, most of the total corporate bond market is in the form of medium- and long-term investment grade bonds, with maturity times in excess of two years.

Still, not all companies and consumers are insulated from higher interest rates. If you bought a new home or car, you would have to bear higher interest costs. The same goes for companies with high debt and low revenue, such as venture capital firms and technology companies, who have been more exposed in our present high-interest rate environment.

Consider also how the strong labor market has contributed to the post-pandemic boom. Most of the year-over-year gains have been in health care, government, and construction. Many of the job gains seen in health care and government have been with health practitioners and social workers. These growth areas are less capital intensive and, by extension, less interest rate sensitive. Construction, meanwhile, is an industry that tends to be more interest rate sensitive but has received ample subsidies through the $400 billion 2021 infrastructure bill. Much of this new spending is merely crowding out more productive private-sector investments over the long run. Even the recent trend of increased immigration, which has improved the labor outlook, could prove temporary depending on the outcome of the upcoming presidential election.

Fiscal Challenges Ahead

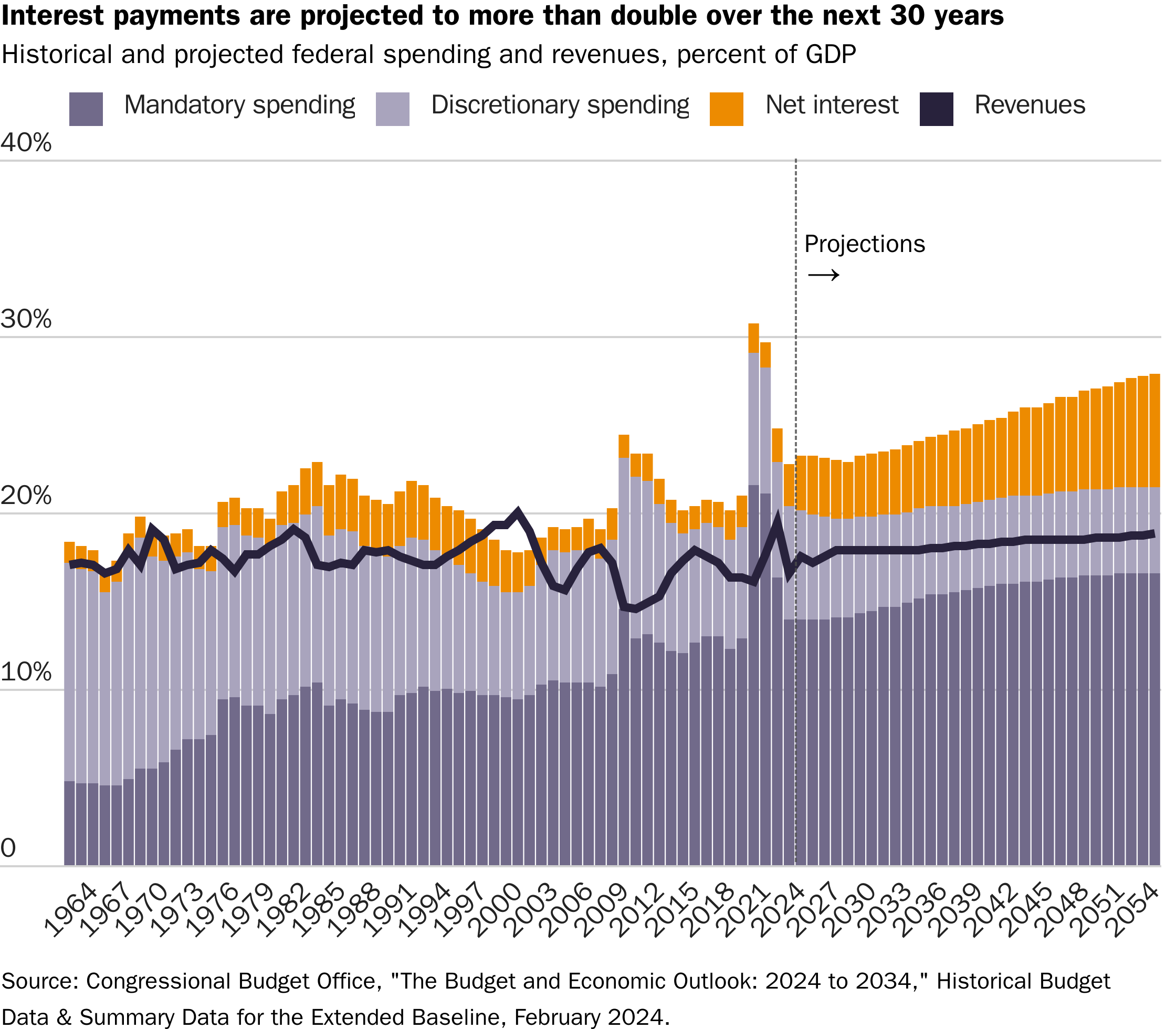

Meanwhile, the US faces a severe fiscal challenge. The US could be entering a new period of persistently elevated interest rates. Returning to the “free money era” of the 2010s seems increasingly unlikely, with the Congressional Budget Office projecting interest rates on 10-year Treasury notes to remain at or above 4% over the next 30 years. Those higher rates will significantly raise the cost of servicing the national debt, accelerating our fiscal decline (see the graph below). As new consumers and businesses enter the market and as existing loans are refinanced, high interest rates will exert increasing downward pressure on the economy, slowing growth and innovation.

The regional banking crisis that occurred last year, featuring Silicon Valley Bank, Signature Bank, and First Republic Bank, illustrates how rising interest rates are already placing pressure on the financial sector. In a new paper, the American Enterprise Institute’s Paul Kupiec warns that waning demand for commercial real estate and high interest rates have made it uneconomical to refinance some properties as existing loans mature, creating a potential for significant bank losses. In the worst case, he argues that we might face a sequel to the 1980s Savings and Loan Crisis and the 2008 Great Financial Crisis.

As the debt burden and interest costs rise, investors will likely become increasingly concerned about the government’s ability to service its debt without inflating away the value of its bonds. A sudden loss of confidence could cause a rapid and spiraling fiscal crisis, wherein bondholders lose confidence in US Treasuries and dump their holdings. Such a scenario could have severe and widespread negative consequences for US economic and national security.

Congress usually waits until the last minute to deal with inevitable issues, including the national debt. The temporary nature of recent economic tailwinds and interest rate insensitivity is another reason Congress should proactively pursue fiscal reforms. More responsible budgetary practices now, including reining in record-high deficits, can aid the Fed in its efforts to tame inflation by ensuring monetary and fiscal policy are working in tandem. It would also signal to markets that Congress is serious about tackling the long-term debt challenge, strengthening the norms that underlie the credibility of US Treasuries. If Congress wishes to get America’s dire fiscal trajectory under control, it needs to start laying the groundwork now. Delaying responsible budget reform until a crisis is on our doorstep puts America’s economic and national security in jeopardy.

The precarious dance between growth and tax burden: a philosophical reflection

In these times of economic upheaval, the article "Will economic growth be short-lived in the face of fiscal challenges?" raises fundamental questions that go to the heart of human society. On the one hand, economic growth, like a bewitching siren, holds us with its promises of prosperity and abundance. On the other, the tax burden, like a menacing specter, hovers above our heads, reminding us of the limits of our wealth and the responsibilities that result from it.

The article highlights the ephemeral nature of current economic growth, fueled by unsustainable fiscal policies and temporary tailwinds. This illusion of prosperity, similar to a mirage in the desert, masks the fiscal challenges looming on the horizon. The meteoric rise of the American economy, like a shooting star, cannot last forever.

The illusion of growth and the burden of debt

Easy access to credit and government spending programs, like deceptive siren songs, lull individuals and businesses into a false sense of security. This deceptive ease, similar to economic opium, masks the risks inherent in excessive debt.

Like a fragile house of cards, current economic growth rests on unstable foundations. The inevitable rise in interest rates, like a glacial winter wind, threatens to collapse this fragile edifice. The crushing weight of the national debt will hamper economic growth and stifle innovation.

The specter of financial crisis and loss of confidence

Rising interest rates, like a threatening storm, could undermine the financial sector, weakening banking institutions and triggering a potential crisis. This crisis, similar to a shipwreck on the high seas, could engulf the economies of individuals and businesses, sowing chaos and desolation.

Losing investor confidence in the government's ability to manage its debt, like a ship losing its compass, could trigger an even more serious financial crisis. This crisis, similar to a devastating tsunami, could devastate the economy and threaten national security.

The philosophical awakening: towards responsible tax management

Faced with these colossal challenges, the article calls for a philosophical awakening, a collective awareness of the need for responsible tax management. This awakening, like the dawn of a new day, must light the way towards a more sustainable and prosperous future.

Deep tax reform, such as a radical transformation, is needed to reduce record deficits and guarantee economic stability. This reform, similar to a makeover, must revitalize public finances and restore investor confidence.

Long-term planning, like a prophetic vision, must guide tax policies, anticipate future challenges and prepare future generations. This planning, similar to a star map, must chart the path to a stable and prosperous future.

The coordination of monetary and fiscal policies, like a harmonious symphony, must guarantee the coherence of government actions and avoid negative contradictions. This coordination, like a well-functioning orchestra, must ensure economic stability and sustainable growth.

Artificial intelligence: a tool for more efficient tax management

Artificial intelligence (AI) offers considerable potential to improve the efficiency of tax management. By analyzing large data sets, identifying suspicious behavioral patterns, and automating tedious tasks, AI can help governments:

Detect tax fraud: AI can analyze tax returns and financial transactions to identify anomalies and inconsistencies, helping to target investigations and deter fraudsters.

Reduce costs: Automating certain tasks related to tax management allows administrations to reduce their costs and free up human resources for more strategic missions.

Finally the article “Will economic growth be short-lived in the face of budgetary challenges? invites us to in-depth philosophical reflection on the links between economic growth, fiscal pressure and future stability.

By recognizing the challenges ahead and adopting responsible fiscal policies, we can navigate the turbulent waters of the global economy and build a more sustainable and prosperous future for generations to come.

Do not forget :

The need for regular breaks: Taking time to reflect and recharge is essential to approaching complex challenges with clarity and insight.

The importance of information: Staying informed about economic trends and technological innovations allows us to make informed decisions and adapt to change.

Openness to innovation: Embracing new ideas and approaches is crucial to finding creative and sustainable solutions to future challenges.

By taking a responsible and proactive approach, we can navigate the turbulent waters of the global economy and build a more stable, more prosperous and fairer future for all.