Debt Digest | US Healthcare Spending: More Money, Worse Results

Debt Digest | US Healthcare Spending: More Money, Worse Results

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

Congress considers stopgap funding package. The House is mulling over a 6-month stopgap funding extension, reports Roll Call’s Aidan Quigley. “The length of the stopgap measure, if enacted, would ensure that lawmakers won’t get jammed with a lame-duck omnibus package right before Christmas, while punting final spending decisions into the new year and a new Congress — possibly with more GOP leverage to shape the outcome.” The continuing resolution (CR) would not have “the steep nondefense cuts that some conservatives have angled for. But House Republicans have struggled to pass their own versions of fiscal 2025 spending bills; just five out of 12 have passed so far, largely defense-related measures.” Discretionary spending cuts are a fiscally sensible objective, but they will not be sufficient to rein in growing deficits, not least because of legislators' worry about proliferating global security threats. Congress inevitably will have to tackle the real fiscal challenge of unsustainable entitlement growth if it wants to stop the exploding national debt. A BRAC-like fiscal commission offers the best chance of doing so.

Is there a right to Social Security? No. As former Cato senior fellow Michael Tanner explained in this 1998 commentary, the 1960 Supreme Court case Fleming v. Nestor established that workers have no legally binding contractual rights to their Social Security benefits. Indeed, only under a privatized Social Security would workers have full property rights in their retirement accounts. For this reason and several others, I’ve argued that Social Security is not an “earned benefit.” Instead, it is an intergenerational transfer scheme, taking money from a younger workforce to finance benefits for primarily elderly retirees. Coming to grips with the reality that Social Security is an income transfer program rather than an earned benefit is necessary to “have a more rational conversation about who should receive how much in benefits, considering their circumstances, without losing sight of how much is fair to ask younger workers to pay to fund those benefits.”

Immigrants improve the fiscal outlook. Per the latest Congressional Budget Office (CBO) Social Security projections, “CBO has reduced its projections of the number of Social Security beneficiaries after 2034, which lowers its projections of long-term outlays for Social Security […] the agency now estimates that half (rather than all) of the people in the United States who are not citizens or legal permanent residents will be eligible for Social Security benefits on the basis of their own work record or that of their spouse.” As Robert Pozen and Charles Blahous explain, “Social Security isn't in trouble because of people crossing the U.S. border. The problems lie in Social Security law itself - specifically, the looming gap between its benefit obligations and its revenue collections. Social Security's finances are actually strengthened by increased immigration - which, contrary to popular myths, would not generally increase crime or reduce employment by native-born Americans.” Over the next 10 years, CBO estimates higher net immigration will boost general revenues by $1 trillion. Read more about how immigration reduces the deficit here.

US status in global financial markets offers extraordinary privilege. “Over the past two decades, the US has actively utilised fiscal policy for macroeconomic stabilisation and transfer policies, leading to a significant rise in public debt levels. Currently, public debt exceeds 100% of GDP. Coupled with rising interest rates, this has raised concerns about the sustainability of US public debt and the government's ability to meet its obligations,” write Jason Choi, Duong Dang, Rishabh Kirpalani, and Diego Perez. Based on a sovereign default model, the country’s role as a safe global asset and reserve currency supplier grants the US an ‘exorbitant privilege’ status, which generates an additional debt capacity of “around 22% of GDP, mostly due to debt being liquid and widely used as collateral. Overall, the US’s status in global financial markets is crucial for debt sustainability, and efforts by other countries to establish competing safe assets could pose challenges to the US’s dominant position.” Likewise, Congress must rein in entitlement spending to prevent fiscal dominance, which could deteriorate the reputation of the US as a guarantor of its credit.

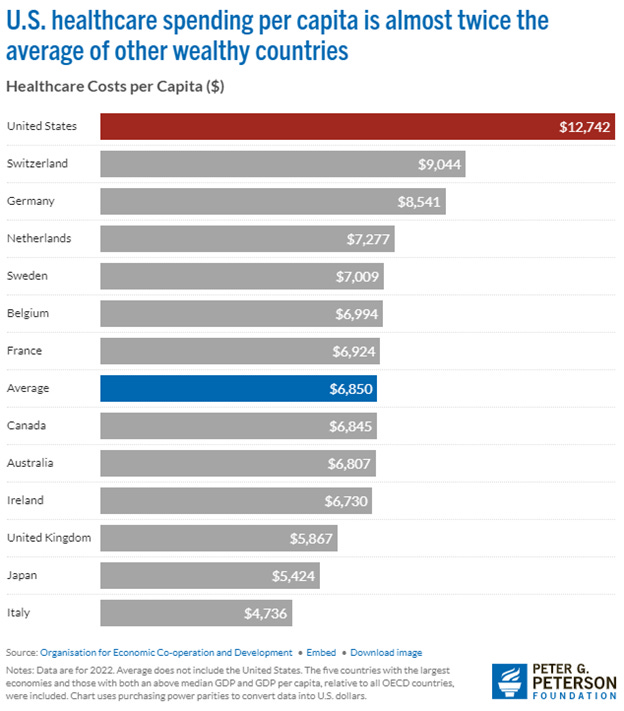

The US spends too much on healthcare. The US spends significantly more than other comparatively wealthy countries, per the Peterson Foundation (see the graphic below). “In fact, the United States spends over $1,000 per person on administrative costs — almost five times more than the average of other wealthy countries and more than it spends on long-term healthcare. […] Higher healthcare spending can be beneficial if it results in better health outcomes. However, despite higher healthcare spending, America’s health outcomes are not any better than those in other developed countries. The United States actually performs worse in some common health metrics like life expectancy, infant mortality, unmanaged diabetes, and safety during childbirth.” As Cato’s Michael Cannon explains, government intervention is a major reason why prices are so high and why quality is so poor. “To improve health care quality and reduce health care prices, state and federal legislators must repeal or drastically overhaul regulations, tax distortions, and entitlement programs that encourage producers to consolidate.”