Debt Digest | The US Debt Crisis is a Bipartisan Problem

Debt Digest | The US Debt Crisis is a Bipartisan Problem

Links & Fiscal Facts

Here are this week’s reading links and fiscal facts:

Both presidential candidates are wrong about Social Security. During the recent presidential debate, candidates were asked how they would save Social Security from insolvency. President Biden stated that making the wealthy "pay their fair share" would be sufficient to save the system. As covered in the last Digest, this solution is mathematically impossible. Former President Trump blamed President Biden’s immigration policies, but Social Security was running cash-flow deficits long before Biden’s term. In fact, immigration could improve the program’s finances, at least over the short-term. As I’ve recently discussed on the NPR Marketplace, presidential candidates’ statements about Social Security mask the complexity of the issue: “I think there’s a real difficulty in talking about Social Security, because there’s been so much storytelling [...] And there’s so many myths out there about how the program works [...] Unfortunately, there is no silver bullet to fixing Social Security that doesn’t involve tax increases or benefit cuts, which is why I think it’s so important to have an honest conversation that there is no free lunch here.”

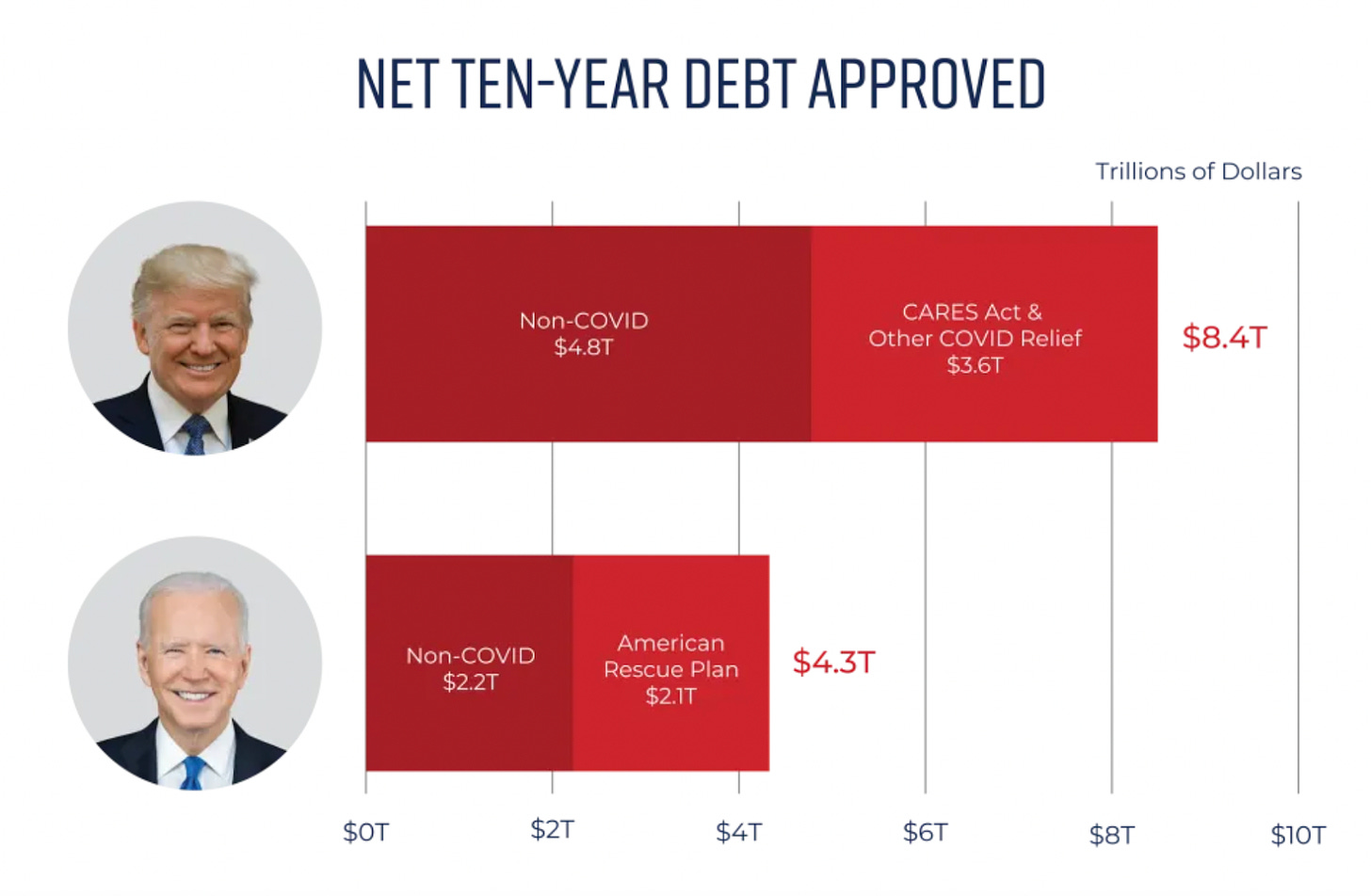

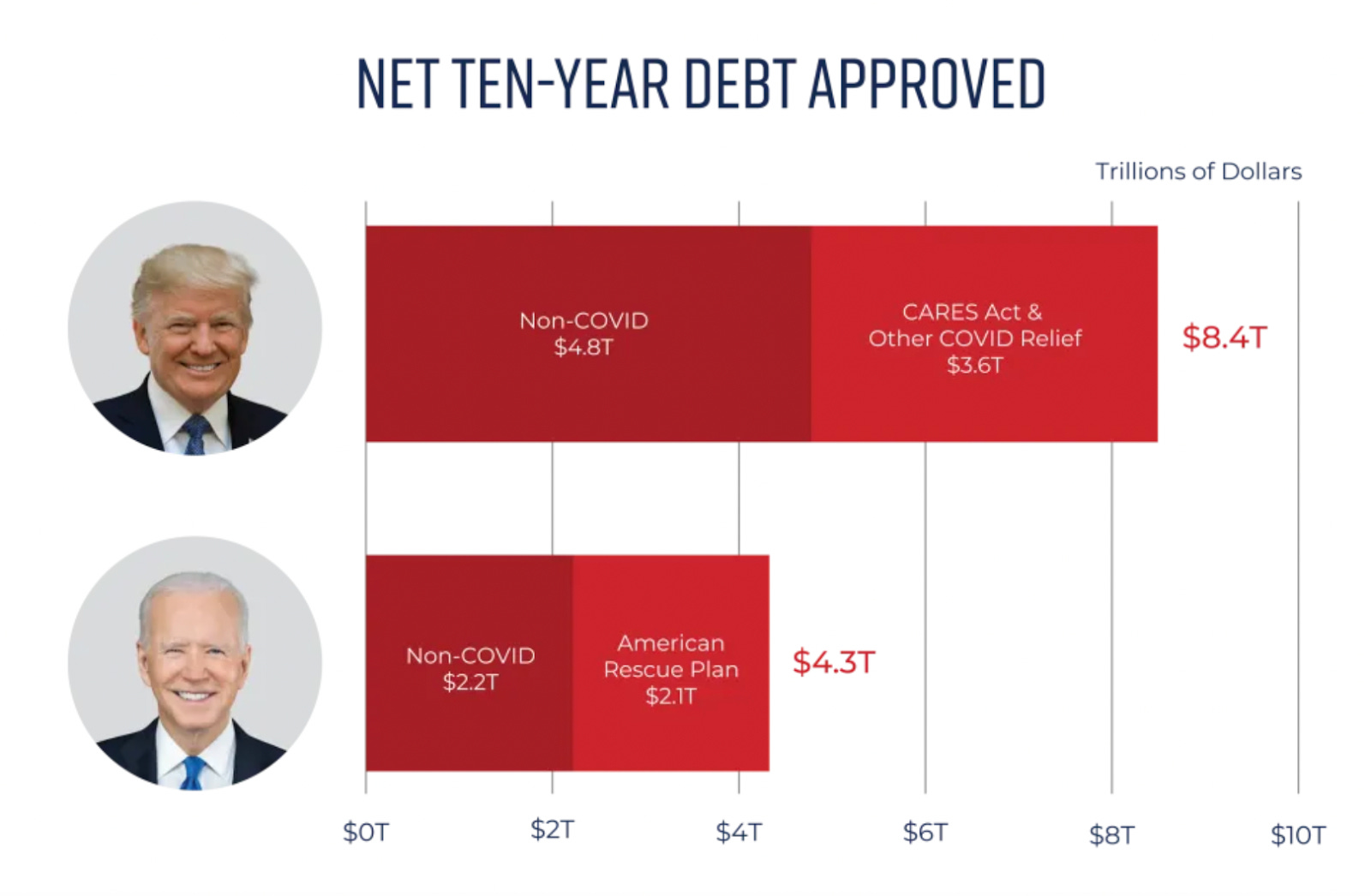

The US debt crisis is a bipartisan problem. The Committee for a Responsible Federal Budget (CRFB) states: “President Trump approved $8.4 trillion in borrowing over a decade, while President Biden has approved $4.3 trillion so far in his first three years and five months in office [see the figure below].” While a significant portion of the debt approved by Trump and Biden is COVID-related, the CRFB correctly points out that “a meaningful portion of this COVID relief was either extraneous, excessive, poorly targeted, or otherwise unnecessary.” The House Budget Committee has criticized some of the figures behind CRFB’s analysis but the big takeaway, that both Presidents are big spenders, remains. Regardless of the outcome of the upcoming presidential elections, as we have previously written, “US legislators should take measures today to stabilize the US debt-to-GDP ratio at no higher than 100 percent of GDP, putting downward pressure on interest rates by reducing spending and addressing unfunded entitlement program obligations.”

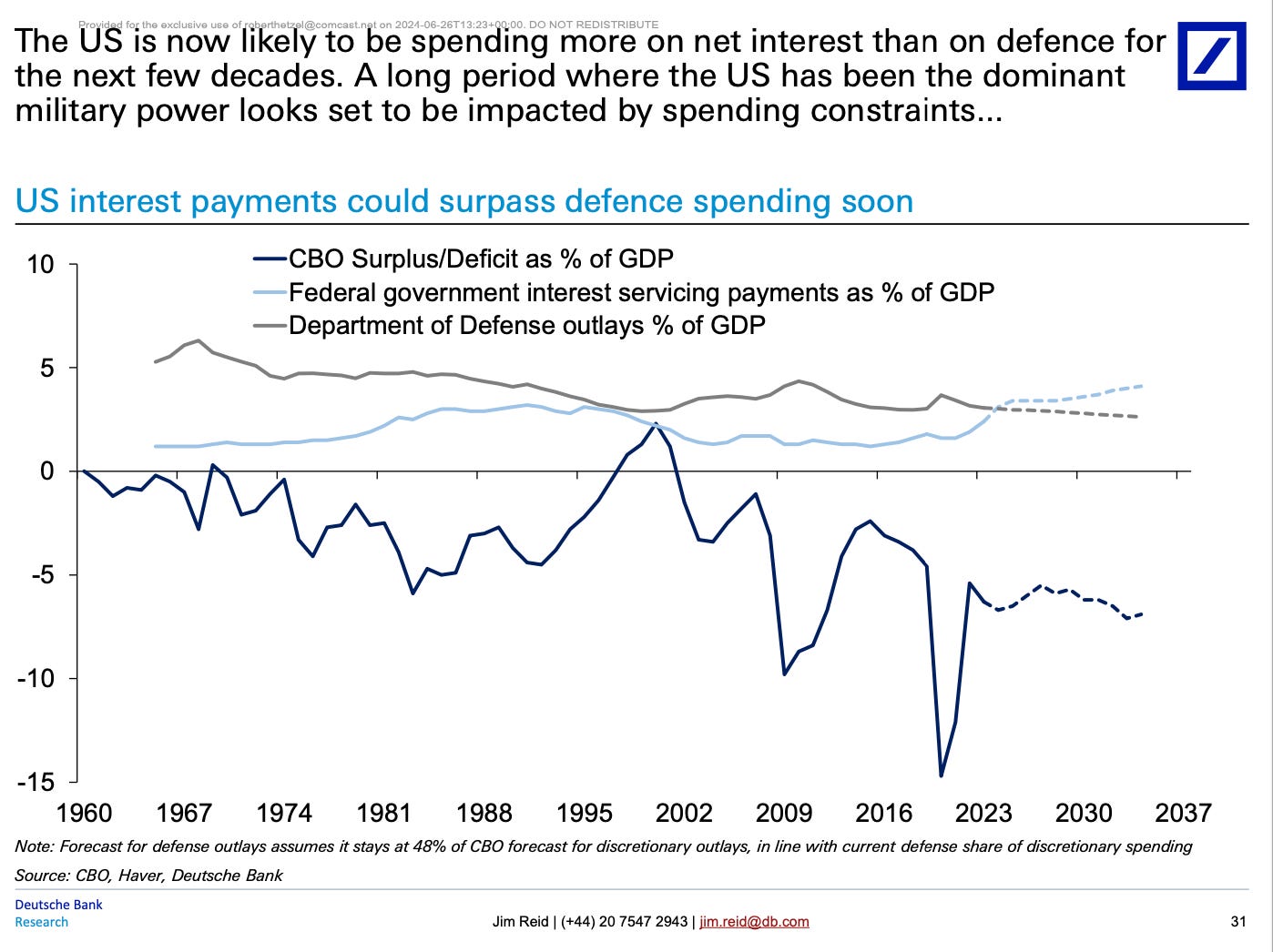

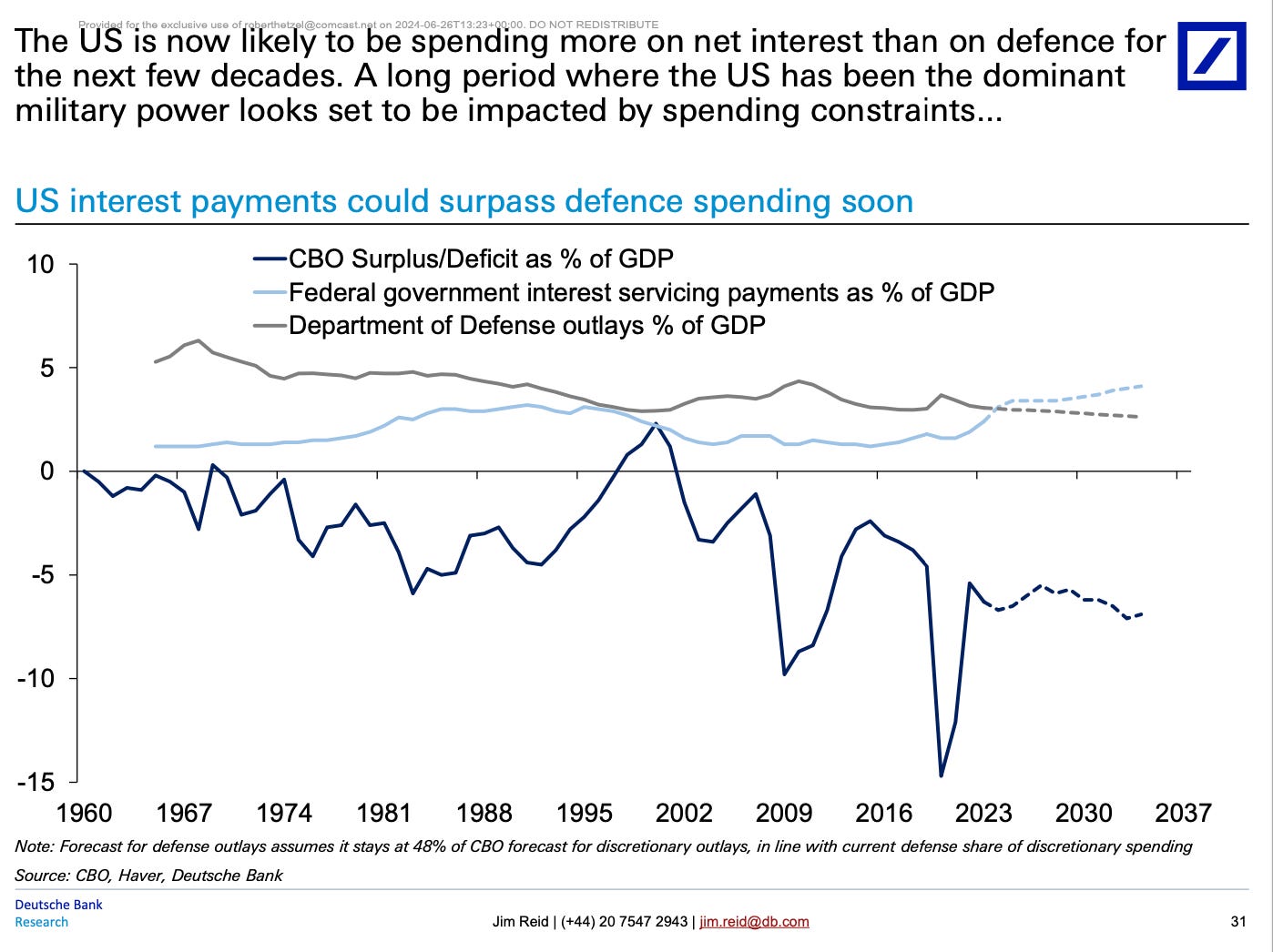

History shows the significant risks of high debt servicing costs. Gerald F. Seib, a visiting fellow at the Robert J. Dole Institute of Politics at the University of Kansas, cites historian Niall Ferguson’s “personal law of history” in his Wall Street Journal essay: “Any great power that spends more on debt service (interest payments on the national debt) than on defense will not stay great for very long. True of Habsburg Spain, true of ancien régime France, true of the Ottoman Empire, true of the British Empire, this law is about to be put to the test by the U.S. beginning this very year.” As a reminder, the Congressional Budget Office (CBO) projects that interest costs will surpass defense spending this year (see the figure below). Moreover, recent historical examples from Greece and the UK demonstrate that an unsustainable debt trajectory can precipitate a bond crisis in unexpected ways. As I have written before: “Should a financial panic ensue, the government has little chance of stopping the flood wave of declining bond market sales, rising interest rates, and pressure to monetize the debt via the Federal Reserve.”

A BRAC-like fiscal commission could stabilize the debt. In her recent article for KSL, Gitanjali Poonia cites our quote: “Romina Boccia and Dominik Lett, budget scholars at CATO Institute, a libertarian think tank, said in an article that a commission is ‘the most promising pathway to overcome the political barriers to reform and avoid a sudden financial crisis and economic decline.’ The only way out is to stabilize debt by ‘reducing spending and addressing unfunded entitlement program obligations,’ like Medicare and Social Security, the researchers wrote.” A BRAC-like fiscal commission would be comprised of independent experts tasked with stabilizing the growing federal debt. See here for more details on the proposed commission. Read here about former House Speaker Paul Ryan’s views on the commission.

Tax cuts should be paired with spending cuts. Alvaro Vargas Llosa, a Senior Fellow of the Independent Institute, writes: “The growth of the U.S. government in modern times is the story of post-WWII America. President Dwight Eisenhower seems to have been the last guy in the post-WWII era who understood that the welfare state, the warfare state, and tax cuts not backed by tough spending cuts are incompatible with fiscally responsible government, or at least with reasonably-sized government.“ Recognizing the need for fiscal responsibility, the new Cato Tax Plan proposes significant tax cuts alongside spending reductions. As Cato’s Adam Michel points out, “Tax cuts without offsetting spending cuts shift the cost of the unfunded spending onto future taxpayers and disguise the actual cost of current government services through so‐called fiscal illusion. Future generations will pay the costs of current government spending through some combination of higher taxes, higher inflation, and slower economic growth.” You can read more about fiscal illusion and how it works, here.