Debt Digest | Avoiding a Shutdown by Setting Up a Christmas Spending Blowout

Links & Fiscal Facts

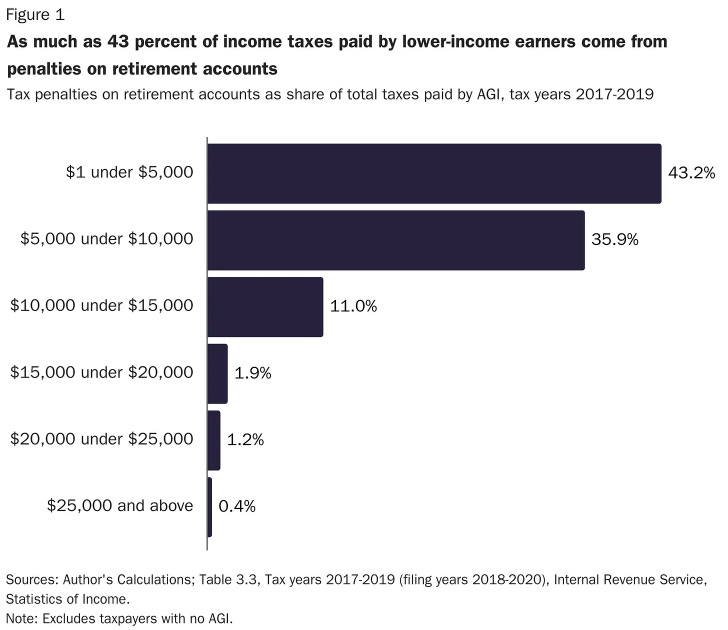

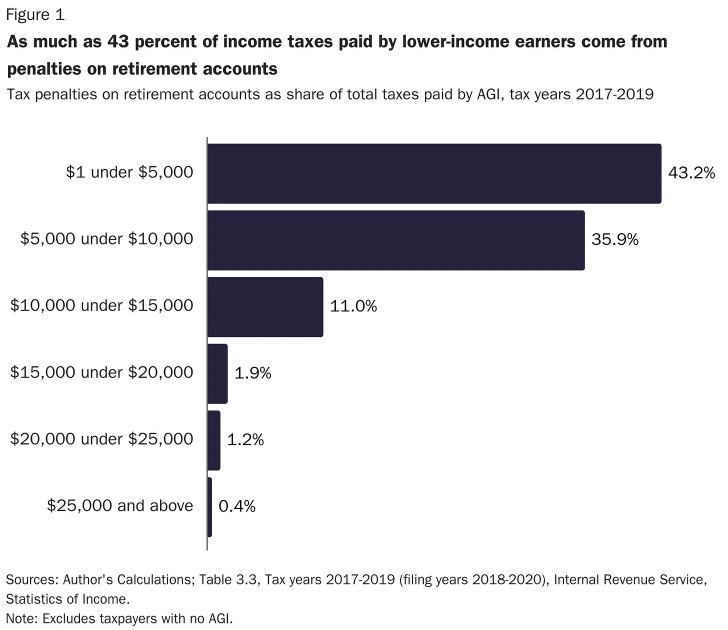

USAs offer flexibility that can boost personal savings. In their recent blog, Cato’s Adam Michel and Joshua Loucks point out that early withdrawal penalties in qualified savings accounts—such as 401(k)s and Individual Retirement Accounts (IRAs)—particularly impact lower-income workers. They explain: “For many young and low-income Americans, the limits discourage them from using the accounts at all. Americans who use these accounts and then have to access their money early for a family emergency or job loss face new layers of taxes. [...] Figure 1 shows that 43 percent of all taxes paid by taxpayers with adjusted gross income (AGI) below $5,000 went to penalties for accessing their own money.” Michel and Loucks propose that Congress introduce more flexible savings vehicles—called universal savings accounts (USAs)—that function similarly to retirement accounts but don’t include tax penalties for early withdrawals. They write: “Removing the tax penalty on all savers is a simple and important step to reduce the tax burden on all Americans, especially those with lower incomes.”

Younger workers are funding the growing benefits of wealthier retirees. Eugene Steuerle from the Urban-Brookings Tax Policy Center and Glenn Kramon from Stanford Business School write: “Most of the taxes workers pay for Social Security and Medicare are not reserved for their retirement but rather pay for current beneficiaries. Like some adolescents who don’t appreciate how much their parents pay to support them, many older Americans don’t seem to appreciate how much more they are taking out than they are put in. A 65-year-old couple with average life expectancy and average household income (about $90,000 in 2023) retiring in 2025 will require $1.34 million to finance their benefits, even though they paid only $720,000. (Numbers are adjusted for inflation.) Younger generations are making up that difference.” As I’ve previously argued, “With younger workers increasingly on the hook for rising benefit costs, effective policy reforms must build on the understanding that Social Security is an income transfer program, not an ‘earned benefit.’”

Population aging is driving Social Security’s growing funding shortfalls. The Congressional Budget Office (CBO) recently responded to questions from Senate Budget Committee leaders about Social Security’s finances. In response to Senator Chuck Grassley’s (R-IA) question about the primary cause of Social Security’s growing funding shortfalls, the CBO answered: “Demographic changes—especially an increase in the number of people age 65 or older relative to the number of people ages 20 to 64—are the largest driver of the increase in Social Security’s outlays relative to the size of the economy since 1984.” To address this trend and strengthen the program’s finances, we’ve suggested increasing the Social Security early and full eligibility ages to 65 and 70. Senator Grassley also asked how Social Security affects the federal debt. The CBO noted that Social Security’s trust fund shortfalls “lead to larger deficits, more borrowing by the Treasury, and an increase in debt held by the public [...]” As I’ve explained, “every time Social Security redeems a bond with the Treasury, Treasury must go out and raise that money from the public, by issuing new government debt.”

House Budget Committee advances key CBO reform bills for fiscal accountability. The House Budget Committee recommended six CBO reform bills to the House, including the Executive Action Cost Transparency Act (H.R.9751) by Rep. Ron Estes (R-KS) and the Stop the Baseline Bloat Act (H.R. 8068) by Rep. Glenn Grothman (R-WI) and Rep. Ed Case (D-HI). The Executive Action Cost Transparency Act would require the CBO to regularly publish cost estimates for executive actions. As Dominik Lett and I noted last week, “Executive spending, unchecked by legislative oversight, threatens both fiscal responsibility and the balance of power. It's on Congress to restore accountability through tighter budget rules, transparent cost reporting, and stronger enforcement of spending controls.” Meanwhile, the Stop the Baseline Bloat Act aims to remove emergency spending from the CBO’s budget baseline, which currently treats such spending as permanent. As I’ve explained: “This statute distorts the fiscal picture, leading to what Dominik Lett and I have called an ‘insidious ratcheting effect,’ where spending is biased upwards as emergency funds inflate the baseline, making it easier for legislators to justify additional spending.”

Congress passes a 3-month stopgap measure, setting up a Christmas funding fight. Last week, Congress passed a stopgap funding measure that was quickly signed into law by President Biden, preventing a government shutdown and extending funding until December 20th. The continuing resolution (CR) is relatively “clean,” increasing base discretionary spending by about $5.6 billion compared to fiscal year 2024. While several proposed “emergency” plus-ups are absent, the bill does include $231 million in new Secret Service funding to provide additional protection for presidential candidates, along with several “spend faster” provisions that allow some agencies to tap into full-year funds at a faster rate than normal. For some programs, such as the Special Supplemental Nutrition Program for Women, Infants and Children (WIC), the “spend faster” provisions could set up bad incentives, increasing the likelihood they’ll ask for (and will likely get) more when it comes time for full-year appropriations. More generally, the CR sets up a December funding fight that in the past has led to Christmas tree omnibus spending bills adorned with unnecessary deficit-increasing provisions. Debt watchers and deficit hawks should be wary. With discretionary spending caps under the Fiscal Responsibility Act expiring next year and debt on the rise, the last thing this country needs is another budget-busting discretionary spending bill.

Does anyone in Congress even discuss this issue anymore ? As best I can tell not much : from either side . (Save for the off chance rhetoric about raising taxes on thr rich or making it more Progressive in its operation ) Alas .

“Demographic changes—especially an increase in the number of people age 65 or older relative to the number of people ages 20 to 64—are the largest driver of the increase in Social Security’s outlays relative to the size of the economy since 1984.”

Q: has someone done the math and verified that this is true? Based on data you provided a few months ago, it seems to me quite possible that the fact that benefits go up with average earnings rather than go up with inflation is likely to be an even bigger driver of the increase in SS outlays over the last 40 years.

(P.S. either way, I support increasing the full benefits retirement age beyond what it is now.)